"Why does India have only two ‘too-big-to fail’ banks? Moody’s raises a valid question")

Global rating agency Moody’s has raised a few questions on the Reserve Bank of India (RBI) decision to award the domestic systemically important banks (D-SIBs) status to only two banking entities. The agency has said the central bank’s approach on D-SIBs or ‘too-big-to fail’ entities is ‘less stringent’ than other jurisdictions, hence credit negative.

Last week, the RBI named the country’s largest lender, State Bank of India (RBI) and ICICI Bank as D-SIBs.

This surprised some banking industry observers since the central bank, in its July 2014 framework for D-SIBs, had said it expects that about 4-6 banks may be designated as D-SIBs under various buckets. This was, however, based on the 31 March 2013 numbers. Moreover, SBI and ICICI Bank were sure picks as they are the biggest banks in the industry.

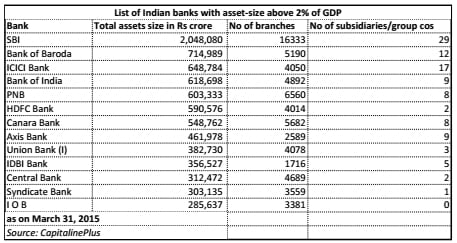

In simple terms, D-SIBs are those interconnected entities, whose failure can impact the whole of the financial system and create instability. The criterion to decide the primary sample of D-SIBs was done by selecting banks with asset size beyond 2 percent of GDP. Going by this methodology, at least 13 banks fall under this category, according to a Firstpost analysis. (See the table)

These include Bank of Baroda, Bank of India, PNB and HDFC. To be sure, the 2 percent cut-off is used to select the primary sample. The RBI would further scrutinise this list of banks based on interconnectedness, lack of readily available substitutes or financial institution infrastructure and complexity.

The RBI can exercise its discretion on the final list and hence the central bank can justify the selection of only two banks from about 27 public sector banks, 19 private sector banks and 43 foreign banks. But, according to Moody’s, the Indian central bank has taken a ‘less stringent approach’ in categorising the D-SIB category.

Central banks world-over began to look at ’too-big-to-fail’ banking institutions closely after the 2008 global financial crisis. In fact, International Monetary Fund managing director Christian Lagarde in March had cautioned that fast-paced financial development in an economy could offer more harm than positives.

Now the question is whether SBI and ICICI are the only two entities to be considered as D-SIBs. This is where Moody’s has raised questions.

The agency has noted the following points:

1) India’s D-SIB framework is less rigorous than those of other jurisdictions;

2) With only two banks in India designated as D-SIBs, the country has the least number of D-SIBs among those that have implemented the framework;

3) The RBI’s capital surcharge is lower at less than 1 percent, and the RBI’s timeline for complying with the capital surcharges is longer, despite the presence of the less stringent capital requirements. Canada and Australia require compliance by 2016, and in Singapore, locally incorporated banks have had to comply with the higher capital requirements since June 2011, Moody’s said.

If one goes by the size and number of subsidiaries/branches, Bank of Baroda is bigger than ICICI with Rs 6.5 lakh crore assets, 5,190 branches and 12 subsidiaries or group companies, whereas ICICI Bank has an asset size of Rs 6.5 lakh crore and, 4,050 branches and 17 subsidiaries/group companies. Wouldn’t a failure of BoB or, for that matter next 3-4 banks by size, trigger a crisis in the sector?

With the D-SIB designation, SBI will have to maintain additional common equity as a percentage of risk-weighted assets of 0.6 percentage points above the minimum required for other banks, while ICICI Bank will need an additional 0.2 percentage points. The additional requirements differ because the RBI classifies SBI and ICICI Bank in different set of systemic importance.

In some sense other state-run banks, would be relieved with the RBI’s exclusion from the D-SIB list, since they are at the mercy of the government for capital. Inclusion as D-SIBs would have meant that they will have to set aside higher amount of capital in the capacity of ‘too-big-to-fail banks’ and closer scrutiny.

They would, perhaps, rather be happy to remain small and lightweight.

(Data support Kishor Kadam)

"Finance Minister Sitharaman tells RBI, regulators to meet fintech startups every month following Paytm fiasco")

"Head-on | From West to India, reversing the brain drain")

"Vantage | Can Paytm still be saved?")

"Vantage | The big message in RBI's Paytm crackdown")

"Finance Minister Sitharaman tells RBI, regulators to meet fintech startups every month following Paytm fiasco")

"Head-on | From West to India, reversing the brain drain")

"Vantage | Can Paytm still be saved?")

"Vantage | The big message in RBI's Paytm crackdown")