"Bank reforms: PM Modi shouldn't repeat the mistakes Manmohan made")

Addressing the Vibrant Global Summit 2017, at Gujarat’s Gandhi Nagar, Finance Minister Arun Jaitley, said the Narendra Modi-government has taken bold steps for the growth of the country and bring in more transparency, echoing the line of Prime Minister Narendra Modi. Yes, Modi government has done much better than UPA-regime to take high-risk reform calls, demonetisation is the biggest example.

The goods and services tax (GST), insolvency code, efforts to rationalise or cut down subsidy burden, bring more transparency in the financial system shows Modi’s reform intent, something which, even his political enemies wouldn’t doubt. But, Modi will risk losing his focus on the bold reform agenda if he fails to address the banking sector reforms beyond what is already done.

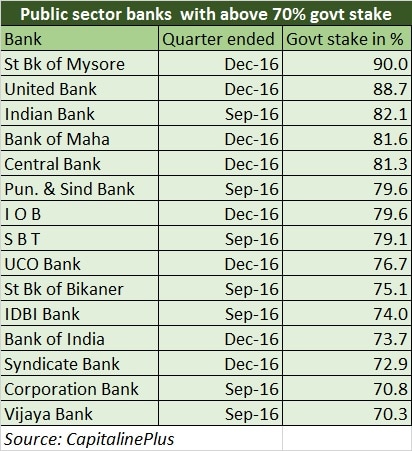

India’s PSU banks, which make up 70 percent of the total banking industry, are in a sad state. Consider this. The state-run banks are neck-deep in bad debts (about 12 percent of their total loans are either bad or being restructured) and are ready with their begging bowls to march to North Block for survival capital. They are unable to fend for themselves–to service their mandatory reserve requirements, bet on higher credit growth and repair their impaired balance sheets. If there is a serious intent to revive the banking sector and the idea is overhauling the banking sector, cosmetic changes will not help.

Following are the problem areas:

Capital The current annual allocation of Rs 25,000 crore under the Indradhanush programme is inadequate to equip the banking system for a higher growth phase in the economy. Sidhharth Purohit, analyst at Angel Broking Ltd, estimates that at least Rs 35,000 crore should be infused in the state-run banks to make them strong institutions and enable these banks aid the economic growth in Asia’s third largest economy.

Under the government’s Indradhanush plan, of the Rs 1.8 lakh crore capital needed by banks under Basel-III, the government has offered to infuse Rs 70,000 crore over four years till 2018-19 and wants the government banks to fend for themselves for the remaining Rs 1.1 lakh crore from the market. This is clearly not enough. Also, how does the government expects that weak state-run banks will find takers? This compounds the problem. So far, there is not much progress on the reform front. That is why the government, the majority owner in these banks, will have to think about infusing them with higher chunks of capital and push the reform button.

Demand revival Capital, however, is only one part of the issue. The bigger problem is that there is no economic activity on the ground at this stage necessitating more capital. So, the government will have to do something to boost demand from companies, while simultaneously recapitalizing banks. The initiatives in the housing sector are welcome step in this direction. Lending rate cuts alone wouldn’t do the trick since there isn’t enough demand for loans, especially from corporations.

Privatisation

Bad loan resolution The ongoing clean up exercise, initiated by the Reserve Bank of India (RBI) under Raghuram Rajan, has helped to dig out much hidden dirt from the bank balance sheets but that isn’t enough. Recognising the problem is one part, the next step is how to deal with it. Recovery of large corporate loans is a nightmare to public sector banks. The debt recovery tribunals have failed to speed up the process. The battle often ends up in courts prolonging the dispute resolution to years. Will the new insolvency code change this scenario is a question one needs to wait and watch. But, one efficient way for the resolution of bad loans stuck in the banking system is by creating a separate entity—bad bank—to deal with this task. All the bad assets in the banks should be transferred to this new entity, whose sole task will be to recover this chunk of impaired assets.

Autonomy in functions By now, there are reasons to believe that the Modi-government has happily inherited the practice of micromanaging banks from the UPA-regime, asking them what to do and what not to do. This is something they should stop immediately. We saw banks being pushed to the corner for Jan Dhan targets, now the latest example came when PM Modi called for a rate cut from banks, in his speech on the new-year eve, which was religiously followed by banks with up to 90 basis points lending rate cuts. This yet again send a wrong signal if the idea is to let banks do their business. If the idea is autonomy in functions, it is not the government but the banks that should take a call on their business. Else, there isn’t any difference between the Modi-administration and what the UPA-governments used to do in the past.

Rating agencies too have repeatedly cautioned that a weak banking sector continues to be a major drag in the India growth story. It is time Modi government pay attention to the warning signals from banking sector which is the backbone of any economy. The latest data shows that bank credit growth slowed to the lowest since 1997 (read the story here ). This should ring a bell to the government about how deep is the pain inflicted by demonetisation resulted cash crunch on economy. Bank credit coming to a grinding halt mirrors the poor economic activity on the ground. Even if this is a short-term phenomenon, the government can’t and shouldn’t ignore the signal.

The bottomline is this: It is even more critical now for the Modi-government pay more attention to the banking sector problems. At the end of its 5-year tenure, banking sector reforms will be watched closely to evaluate this government’s willingness and ability to undertake ‘bold’ reforms. The UPA, under Manmohan Singh, failed to initiate bold reforms in the banking sector. Narendra Modi shouldn’t repeat the mistake.

(Data support from Kishor Kadam)

For full coverage of Union Budget 2017 click here .

"India’s defence aatmanirbharta has the potential to power its global ambitions")

"FirstUp: PM to unveil Deendayal statue, Nobel nominations out... Today's news")

"UPI in UAE: The changing face of cross-border payments")

"This Week in Explainers: How India joined elite aircraft carrier club")

"India’s defence aatmanirbharta has the potential to power its global ambitions")

"FirstUp: PM to unveil Deendayal statue, Nobel nominations out... Today's news")

"UPI in UAE: The changing face of cross-border payments")

"This Week in Explainers: How India joined elite aircraft carrier club")