"How to keep your retirement finances on track")

By Ranjeet S Mudholkar

Retirement in the general terms refers to the end of working life of an individual, called in other words in organised sector as superannuation. While planning for a happy retirement is a necessary part of the financial life of an individual, there are two phases involved in the process.

1. Accumulation Phase

2. Withdrawal Phase.

Accumulation phase is the period in the working life of the individual when he/she is working and regular contributions are being made towards the retirement corpus. This should be done as per the strategy charted out in a well drafted financial plan in consultation with a financial planner.

It must be kept in mind all the time that the withdrawal phase is as important as the accumulation phase. It is equally important to use the corpus judiciously in a phased manner with a clearly defined strategy so that one does not outlast the corpus and its invested returns.

With the improved health care facilities and above average hygiene factors, the life expectancy and the average age as per Indian demography, both are on a rise it is important for one to secure the well being of self and the dependents during the non earning period of the life. As this trend continues there is a growing requirement to take measures immediately to sustain during the prolonged retirement period due to the factors mentioned above. As per Project OASIS report estimate, number of aged in the country would be close to 17.9 Crore which would be 13.3 percent of population by 2026.

Thus the onus for providing for oneself comes on the individual himself, thus it is important to ensure that the amount of money that is being saved and invested is done in a prudent manner. These investments in addition to providing for sustenance during retirement shall help one on availing tax benefits during the working life of an individual.

Retirement Schemes like Public Provident Fund(PPF) and National Pension System (NPS) get benefit under section 80C of Indian Income Tax Act, 1961. Investment in pension plans of Insurance companies is also exempt under section 80C of the said act. Post Clearance of pension bill in the parliament, the retirement market is expected to grow at a faster pace with more innovative products expected to be introduced.

The expenses required after retirement will depend upon the income replacement levels required. The corpus accumulated for the purpose of retirement needs to be spent according to a well drafted strategy. As an example if an individual has Rs 1 crore accumulated in his retirement corpus and he wants this amount to last for 25 years then on an average he needs to spend 4 percent of the corpus every year as per the wisdom guided by conventional mathematics. But the requirement is not going to be the same as there would be inflationary pressure on the expenses and on the other side the invested corpus will be able to generate some returns as it would be invested in some low risk asset classes during the period.

Analysing the same, one could arrive at an optimum withdrawal rate to ensure that the corpus lasts if the inflation adjusted annuity is drawn from the corpus invested at slightly above the risk free rate of return. Considering the withdrawal rate of 4 percent of the corpus to begin with and drawing 5 percent inflation adjusted annuity invested at 6 percent, the corpus would last nearly 28 years. This leaves a balance of more than Rs 45 lakh at the end of 25 years to be bequeathed. There can be many similar things which are needed to be taken care in consultation with your planner.

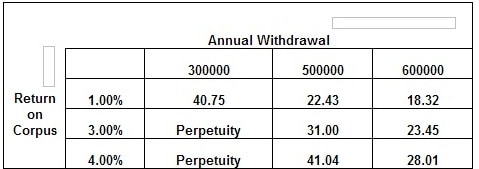

The table below gives various scenarios for which the corpus of Rs.1 crore can last for various different periods based on the spending pattern of the investor and the expected return on corpus and thus clearly illustrating the point about the importance of withdrawal management. ( See table )

The table gives a clear sensitivity analysis on the varying return on corpus at different level of withdrawals with an initial corpus of Rs.1 crores, there are other parameters which can also vary and thus drafting a strategy in consultation with an expert is warranted.

If an individual wants to leave the corpus for the heirs, at the same time ensuring that retirement needs are also taken care of , then the withdrawal needs to be equal to or less than the expected return generated during the period. In this case the required corpus would be more than in case of an annuity. The third and fourth in the second column of the table illustrates the point where the withdrawals are equal to or less than the expected return generated during the period.

Not being able to plan properly can lead to two scenarios

1. Shortfall in the expenses at an advance age.

2. Major portion of corpus lying idle and outliving the investor

Second scenario may still be managed but the first scenario is a situation which should be avoided at any cost. The effort towards the same should begin far earlier in the initial stages of one’s career or even if postponed then mid career is the latest stage when it is feasible to plan for retirement. However it is crucial to note here that retirement plan is a part of Financial Plan only and withdrawal management should be undertaken in consultation with an expert like a Certified Financial Planner (CFP) professional at the time of financial plan construction. This will ensure that the corpus accumulated at the time of retirement is available throughout the retirement period and the individual is not in shortage of funds and not dependent on anybody as well.

Ranjeet S Mudholkar, is Vice Chairman and Chief Executive Officer, Financial Planning Standards Board India (FPSB India). The views expressed here are personal, and do not necessarily represent that of the organization.

"Money Can Buy Happiness: Why married couples who combine finances stay together longer")

"Explained: Why US Senator Dianne Feinstein's absence is becoming a major issue for Democrats")

"Shadow Warrior | SVB collapse: How system-wide problem created by Fed led to US' second-largest bank failure")

"How the battle over retirement in France has become an identity issue")

"Money Can Buy Happiness: Why married couples who combine finances stay together longer")

"Explained: Why US Senator Dianne Feinstein's absence is becoming a major issue for Democrats")

"Shadow Warrior | SVB collapse: How system-wide problem created by Fed led to US' second-largest bank failure")

"How the battle over retirement in France has become an identity issue")

{kind=link}