"The Great Indian NPA Mess: Banks, govt and industrialists worked together to kick bad loans can down the road")

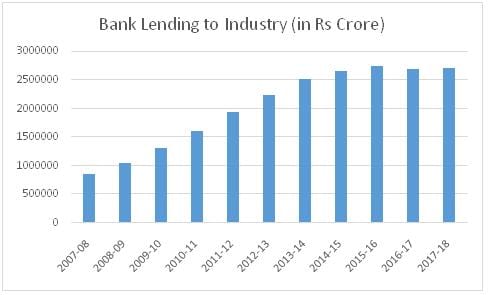

Editor’s note: A political blame game is on after the recent revelations of former Reserve Bank of India (RBI) governor Raghuram Rajan to a Parliamentary panel about the origin of the bank NPA (non-performing assets) mess. About 90 percent of NPAs in India’s banking sector is on the books of state-run banks. This is the third part in a series in Firstpost where experts analyse the issue. In the aftermath of the financial crisis that broke out in 2008, the Western world discovered the work of the economist Hyman Minsky. It’s time that India did as well. Minsky had put forward the financial instability hypothesis. The basic premise of this hypothesis is that when times are good, there is a greater appetite for risk and banks are willing to extend riskier loans than usual. And once the banks are ready to make riskier loans, the quality of their lending automatically comes down. This ultimately creates a problem. Or to put it simply, stability breeds instability. This is clearly how the Indian banks ended up with all the bad loans that they have over the last few years. Bad loans are loans which haven’t been repaid for a period of 90 days or more. As Raghuram Rajan, former governor of the Reserve Bank of India put it in a recent note to the Chairman of the Parliament Estimates Committee, Murli Manohar Joshi: “A larger number of bad loans were originated in the period 2006-2008 when economic growth was strong, and previous infrastructure projects such as power plants had been completed on time and within budget. It is at such times that banks make mistakes. They extrapolate past growth and performance to the future. So they are willing to accept higher leverage in projects and less promoter equity.” [caption id=“attachment_5094841” align=“alignleft” width=“380”]  File image of Prime Minister Narendra Modi. Courtesy- BJP twitter[/caption] Basically, a lot of loans to industry were made by banks before 2008, when the going was good. And this is when the quality of lending fell dramatically. Initially, banks only lent to businesses that were expected to generate enough cash to repay their loans. But as time progressed, the competition between lenders increased (i.e. the different banks) and caution was thrown to winds. An era of easy money was unleashed and money was doled out left, right, and centre. Of course, what helped was the fact that the demand projections of projects for which money was being lent, were also pretty good. As Rajan put it: “Indeed, sometimes banks signed up to lend based on project reports by the promoter’s investment bank, without doing their own due diligence. One promoter told me about how he was pursued then by banks waving checkbooks, asking him to name the amount he wanted.” Such was a rush among banks to lend money. Normally anything like this doesn’t end well. And India was no exception to this. In fact, as of 31 March 2018, the total bad loans of banks stood at Rs 10,35,528 crore or 11.6 percent of the total advances made by these banks. Public sector banks constitute a bulk of these bad loans. The total bad loans of these banks as of 31 March 2018, amounted to Rs 8,95,601 crore or around 86.5 percent of the total bad loans of banks. In fact, 15.6 percent of advances made by public sector banks have been defaulted on. The Reserve Bank of India (RBI) publishes the data for the total lending carried out by banks to industry, every month. The trouble is that this data is available only from March 2008 onwards. Given this, we don’t have any direct way of verifying how much lending was carried out by banks to industry, between 2006 and 2008, which is the period during which things started to go wrong. Nevertheless, what we can take a look at is the non-food credit given out by banks. Banks lend money to the Food Corporation of India and other state procurement agencies to carry out their procurement operations, where they buy agricultural produce directly from the farmers. What is left after this lending is referred to as non-food lending. Between April 2005 (the start of the financial year 2005-2006) and March 2008 (the end of the financial year 2007-2008), the total non-food lending of banks went up by 119 percent to Rs 23.17 lakh crore. This couldn’t have happened without the loans to the industry going up at a good pace during that period. Of course, all this money was lent to the industry at a time when the going was good. And given that the demand projections were very optimistic. The global financial crisis started in 2008 and this led to the economic growth falling to 3.9 percent in 2008-2009, this after three years of greater than 9 percent growth. In 2009-2010 and 2010-2011, government spending pumped up growth again. But by 2011-2012 onwards slow growth returned. As Rajan puts it: “Strong demand projections for various projects were shown to be increasingly unrealistic as domestic demand slowed down." Also, what did not help was the lack of decision making on the government front, which led to a slowdown in projects. As Rajan puts it: “Once projects got delayed enough that the promoter had little equity left in the project, he lost interest.” This is where things went from bad to worse. Take a look at Figure 1, which basically plots the total loans given by banks to industry to over the years.

_(Source: Reserve Bank of India)_

The bank lending to industry between the end of March 2008 and end-March 2014, went up by 193 percent to Rs 25.16 lakh crore. So post-2008, lending to industry continued at a very fast pace. What was happening here? Basically, everyone, the bank, the borrowers and the government, were kicking the can down the road.

As Rajan puts it: “It was in everyone’s interest to extend the loan by making additional loans to enable the promoter to pay interest and pretend it was performing. The promoter had no need to bring in equity, the banker did not have to restructure and recognize losses or declare the loan NPA and spoil his profitability, the government had no need to infuse capital.”

This was the period when the banks should have actually been looking to genuinely restructure these loans to industry. They should have written-off loans they knew they were not in a position to collect. Further, they should have insisted on the borrowers bringing in more equity (i.e. their own money) into the project. This was clearly not possible without the bank being in a position to “threaten promoters, even incompetent or unscrupulous ones, with loss of their project”. What happened instead was that everybody got busy running a Ponzi scheme. The banks gave fresh loans to promoters, the promoters used the fresh loans to repay the old loans and the governments (both UPA and NDA) looked the other way. The profits that the banks generated during this period was illusory because it was their own loans being returned to it. The bank loans to industry peaked at Rs 27.31 lakh crore as of March 2016. The RBI started a crackdown on the bad loans sometime in early 2015. There were cases of crony capitalism as well. In several cases (in particular real estate project), the promoter simply siphoned off the bank loans. Of course, the problem could not be perpetually kicked down the road, and we now have one big problem, which the Narendra Modi government is trying to postpone further by merging different public sector banks. The trouble is bringing two rotten eggs together is only going to lead to another rotten egg. (The writer is the author of the Easy Money trilogy) Read Part 1 here: UPA's sins were of commission while NDA's are of omission Part 2: Bad loans can snowball into banking crisis, Arun Jaitley's solutions has political overtones

"US ready to ‘impose costs’ on Russia if war in Ukraine drags on, says Hegseth")

"US tells Hamas to stop violence against Gaza civilians and disarm 'without delay'")

"China seizes 60,000 maps mislabelling Taiwan, omitting South China Sea islands")

"Syria’s Sharaa pledges to honor Russia ties, seeks economic and military support in Kremlin visit")

"US ready to ‘impose costs’ on Russia if war in Ukraine drags on, says Hegseth")

"US tells Hamas to stop violence against Gaza civilians and disarm 'without delay'")

"China seizes 60,000 maps mislabelling Taiwan, omitting South China Sea islands")

"Syria’s Sharaa pledges to honor Russia ties, seeks economic and military support in Kremlin visit")

](https://images.firstpost.com/wp-content/uploads/2018/09/Modi-banks-BJP-twitter-380.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2018/09/chart1.jpg){kind=link}