"Demonetisation is India's move to less-cash; banks must seize the moment")

In the 21+ odd days post de-legalisation of old high denomination currency – Rs 500 and Rs 1000, there is one clear narrative that has emerged. India is now being catapulted into a less-cash (not cashless) economy. This tectonic shift should also promote the growth of financial inclusion in leaps and bounds. These are early days. The long war for less-cash has just begin. If India has to win this war, it is imperative that banks use the power of their franchise to own and define the narrative. [caption id=“attachment_3119004” align=“alignleft” width=“380”]

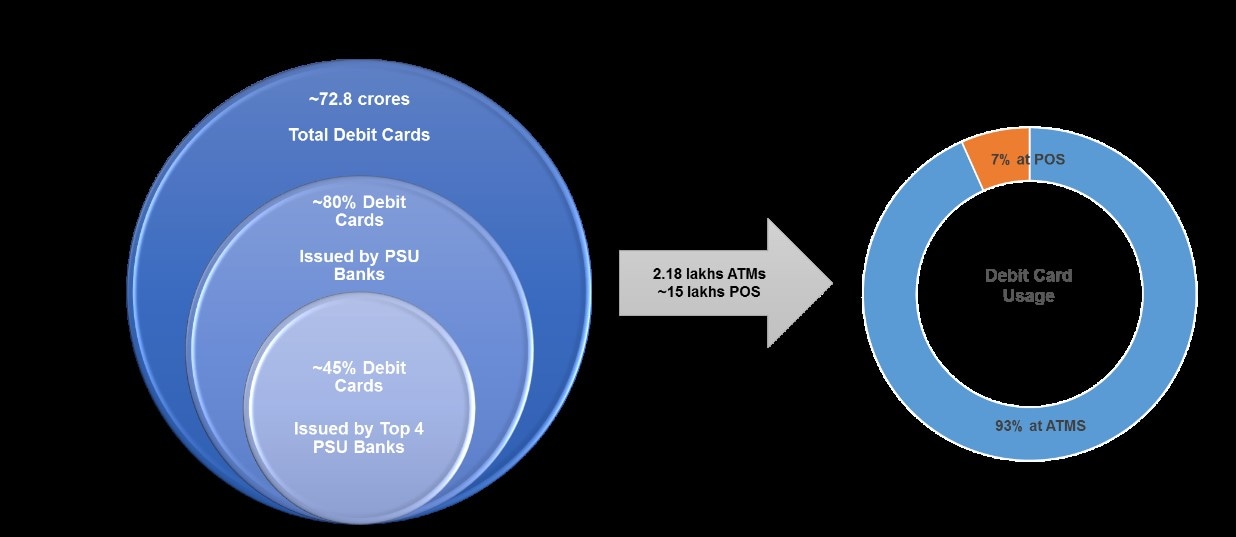

Reuters[/caption] There will be many pillars of the banks’ action strategy for India’s march to less-cash and to drive electronic payments. This note specifically addresses the role of cards (including direct electronic banking transfers by individuals in as much as they are facilitated by cards) across payment channels in this move to less-cash. Cards are an important cog in the wheel as they can replace cash in transactions from consumers to businesses and consumers to other consumers for transfer of funds for personal or business reasons. They are also the instruments that are used to load mobile wallets (hopefully cash will become less!). Basic facts Let us peruse some statistics and facts: • There were ~72.8 crore debit cards and ~2.68 crore credit cards in India as at the end of

September 2016. ~80 percent of these debit cards are issued by PSU banks. The top 4 PSU banks – SBI, PNB, BOI and BOB account for ~45 percent of all debit cards. • As on 23 November 2016, there were 25.68 crore

Jan Dhan accounts. 76 percent of these accounts had an associated RuPay debit card. • There were 2.18 lakh ATMs and ~15 lakh POS terminals as at the end of September 2016. • The cards (especially debit) are used primarily at ATMs.

Data courtesy: RBI, All cards may not active – these are cards issued. • At the end of 2015, compared to ~60 crore cards in India, China would have had a staggering ~4200 crore cards. Even if we account for population and demographic differential, the

gap is staggering. • India has a fully functional indigenous cards network – RuPay – launched by NPCI in 2012. The National Unified USSD Platform (NUUP) is also live. • As per an eMarketer study, the number of mobile users who will be using a mobile messaging app at the end of 2016 will be ~13.3 crore. • India should touch the 50 crore internet users mark in 2017. Important note – Number of cards and number of users do not suggest unique individuals as there may be multiple holdings by one individual and should be discounted when perusing statistics. Have cards will not use! Some prima facie conclusions: • Low card penetration and inadequate POS machines are well acknowledged impediments to the low levels of card usage. However, inactivity of cardholders either due to lack of knowledge and/or due to propensity and the merchant (seller’s) willingness to accept are also critical factors. • If there are only 13.3 crore users who use a messaging app, it is unlikely that a significantly higher number will be more comfortable in using their mobile phones to transact. So mobile payments and mobile wallets while very important drivers, have limitations in terms of reach. • As of today, it is the banks and especially the top 4 PSU banks who have the sheer strength of numbers to drive this move to less-cash. The cards issued by them are already out there. They has to be put to work now. Simple equation, complex eco-system

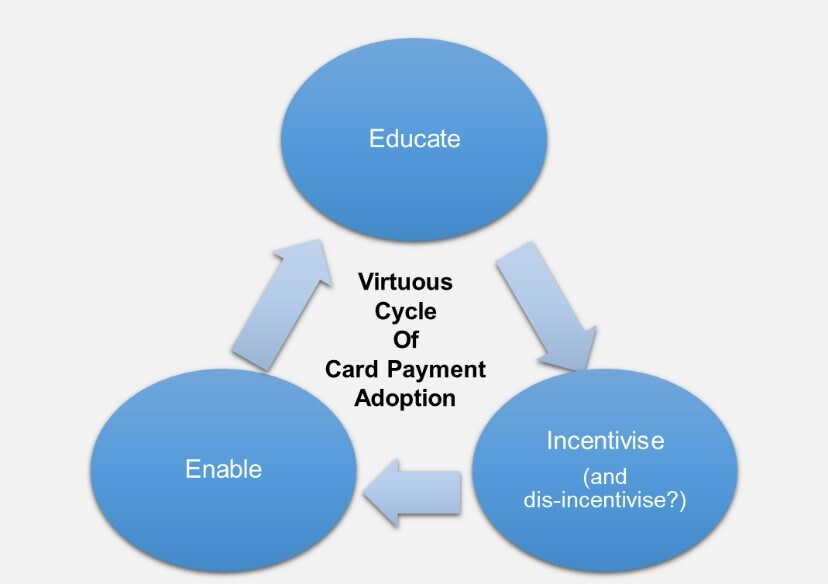

- Robustness implies reliable and secure. Reliability will come from a better telecom network, better maintenance and servicing and building acceptance systems that are scalable. Security is a subject by itself but suffice to say that banks have to not only to beef up security systems but also build trust with both merchants and card holders

- Penetration of acceptance infrastructure is key. It is both horizontal – across consumption categories and vertical – across urban and rural and across merchant sizes. As of today, penetration even beyond metros and Tier I cities is a challenge.

- Acceptance has to be both digital and physical - we need more POS machines and more payment gateways.

- It should be simple and efficient to accept non-cash payments.

The above will require both investment and innovation. A recent study by Visa pegged the cost of increasing POS terminals and merchant and customer acquisition for banks at Rs 1,300 crore over the next five years. Hackneyed as it may sound, innovation at all points of the value chain is absolutely essential. For example, the Visa report assumes the cost of a POS terminal at Rs 8,000–Rs 12,000 exclusive of taxes. It is virtually impossible to penetrate deep with these upfront costs of acceptance. • Increase card penetration. While each citizen may not need a suite of cards, each Indian needs at least one for sure. We are miles away from the fulfilment of that dream right now. 2. Educate This is the most ignored and the most under-rated element of the three pronged strategy. As discussed earlier, a significant number of buyers and sellers shy away from using cards simply because they don’t know how to use them or they believe that cards are inconvenient, not easy to use and not secure. All these issues can be addressed by education and communication. Some critical elements of the education and communication strategy will be: • ATM card = Debit card. ATM pin = Debit card pin. • Getting a new pin is easy – these are the steps. • Cards are secure. This is the way to ensure your security. • Your card has multiple uses – pay bills, book tickets, shop, transfer money, load wallets (how to get your wallet from the bank), withdraw cash, etc. • Where can you use your card – physical establishments, online (how), mobile. Education and communication must be: • Functional and not just emotional. • Usable – Step by step and clear. • Multilingual. A branch manager at a PSU bank remarked– ‘If instructions are in english, they might as well be in greek…’. It may sound radical but in the short to medium term, banks will have to target most of their advertising, PR and communication to customer education. Customer education is going to be as important as customer service, if not more. 3. Incentivise This is the elephant in the room and needs to be addressed. Notwithstanding other enabling factors, incentives have been a key driver in the rapid adoption of well-funded private mobile wallets and can go a long way in positively influencing the propensity to use cards. The primary ecosystem participants outside the buyers and sellers viz. issuing banks, accepting banks, card associations (primarily Visa, MasterCard and RuPay India) and the government will have to arrive at a solution and only one participant cannot bear the burden alone. Incentives are needed in the following broad areas: • Merchant discount rate for sellers’ and convenience fees/surcharge for buyers. • Cash back or other forms of direct customer benefits for recurring and essential categories of spends (this is well understood now). • Upfront setup costs for sellers moving in to the card acceptance fold for the first time. Disincentives may come in the following forms: • Caps on transaction limits by cash. • Additional surcharges and/or fees (inconvenience fees (?)) to be levied for cash transactions in certain categories. A word of caution – surcharges and fees can be harmful if used indiscriminately as history suggests and have to be used sparingly and in a calibrated manner. Carpe diem! The discussion above is neither exhaustive nor path-breaking but to reiterate there are two clear messages: • Banks (especially the PSU banks and especially the top 4) will have to play a pivotal role in India’s quest for a less-cash future. • Both a less-cash future and banks playing a pivotal role in this era of fintech are not utopian dreams. PSU banks have done the heavy lifting for years and now it is time for them to reenergise and reactivate their biggest asset – their massive customer base. We are living in times where less-cash has become a dominant theme and is being pushed relentlessly thanks to political will. Perhaps most importantly there is a sense of urgency in the system, there is a genuine need, desire and willingness to move to a less-cash future. It seems that many stars have finally aligned. Of course, the task at hand is not easy – it is gargantuan. Banks will need to take control of the narrative and push themselves to be in front of the consumers and merchants and to be at the forefront of the less-cash movement. They need to invest behind the payment infrastructure needed, ensure that consumers/merchants see value in paying/accepting cards and innovate endlessly. Probably there is one more change in narrative that is needed…banks (especially large PSU banks) need to be seen, heard and promoted as leaders who can truly lead the nation to a less-cash future. This is their moment and the banks need to seize it! (The author is an independent business and strategy consultant and mentors startups. She has held leadership positions at the Tata Group (TAS), Citibank and Network18.)

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

](https://images.firstpost.com/wp-content/uploads/2016/11/DebitCard380_ATM_Reuters1.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2016/12/chart1.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2016/12/chart3.jpg){kind=link}