"Why Chinese slowdown will impact world and India")

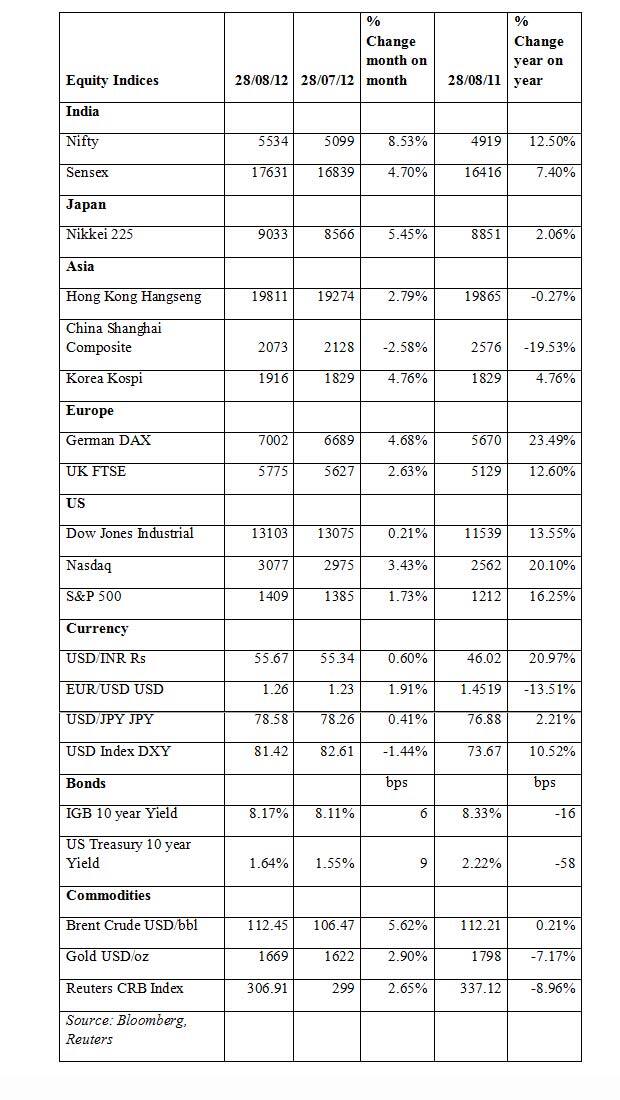

China’s benchmark equity index, the Shanghai Composite Index (Index), is the worst-performing equity index on a year-on-year basis as of end-August 2012. The index has lost 19.5 percent against the positive performance of other major global indices. The only other major market that has not given positive returns is the Hong Kong equity index, the Hangseng, which has given marginal negative returns over the year. ( See table )

In comparison to China and Hong Kong equity market performance, the Sensex and Nifty have given returns of 7.4 percent and 12.5 percent respectively on a year-on-year basis. The US equity index S&P 500 has given returns of 16 percent and the German equity index Dax has given returns of 23 percent. Why is China the worst-performing equity market globally and what does it mean for India and other equity markets that have done well on a year-on-year basis?

[caption id=“attachment_436315” align=“alignleft” width=“380”]  The currency could be a factor in China’s equity market underperformance on an absolute basis. Reuters[/caption]

Currency factor

The currency could be a factor in China’s equity market underperformance on an absolute basis. The renminbi (CNY) has hardly moved against the US dollar (USD) on a year-on-year basis with the CNY gaining 0.6 percent against the USD over the year as of end August 2012. On the other hand, the Indian rupee (INR) has lost 21 percent and the euro has lost 13.5 percent against the USD over the year.

Hence, an FII investing in USD in the markets of China, India and Germany has, on a currency-adjusted basis, lost 19 percent and 8 percent in China and India (taking the Nifty performance of 12.5 percent gains) while the FII has gained around 10 percent by investing in German equities. The US equity markets have given the best return on a currency-adjusted basis as the USD has strengthened against the majors.

The currency factor is applicable only to FIIs investing in USD in foreign equities. The local investor in China has suffered losses while in India, US, and Germany the local investor has gained. Hence, the poor performance of China’s equities is a worry factor for global equity markets as the performance has some fundamental reasons behind it.

China’s economy is facing many issues

China is seeing growth slowing down with GDP growth for the second quarter of 2012 coming in at an annualised rate of 7.6 percent, the slowest growth rate seen since the first quarter of 2009 and the sixth straight quarter of fall in GDP growth. China accounts for around 20 percent of the world’s economic output and a fall in economic growth in China does have repercussions globally.

China was facing an inflationary threat in 2011 with inflation touching multi-year highs of 6.4 percent in June 2011. The country faced a property bubble with real estate prices soaring by 100-150 percent in the 2007-2011 period and bank loans to real estate were under threat on the prospects of the bubble bursting. Property prices have come off over the last one year but given the weak economic growth in China, banks still face issues of real estate loans turning bad.

China’s corporate profits are reflecting the equity market pessimism with industrial group profits down 2.2 percent in the first half of 2012 against a 29 percent growth seen in the first half of 2011.

The eurozone sovereign debt crisis has affected China’s exports with just a 1 percent growth in July 2012. Exports contribute close to 30 percent of GDP and any export growth slowdown will hit the economy hard.

China has a tough task ahead. It has to revive its economy without making overinvestments as many of its past investments are hanging on bank books as potential non-performing loans. Local governments borrow from banks to invest in infrastructure to show growth and in such cases economics does not come into play. Chinese banks are sitting on close to $ 1.7 trillion of local government debt, which accounts for 27 percent of GDP.

The one positive factor for China is inflation, which has come off to below 2 percent levels as of July 2012 from last year’s levels of 6.4 percent. China can cut rates and give more funds to banks by reducing reserve ratios. China has cut rates twice in 2012 and has reduced bank reserve ratios by 150 bps over the last eight months. However, given the excessive lending by banks to real estate and infrastructure, rate cuts may not help as banks worry about bad loans.

How will China’s weak equity markets affect global markets and us?

The sharp outperformance of global and Indian equities over Chinese equities in local currency terms indicates that the problems in China are much more than the problems across the globe. The question is will China’s problems affect other economies? China’s issues may or may not affect other economies negatively. On the positive side, weak Chinese economic growth helps keep commodity prices stable (the Reuters CRB commodity index is down 9 percent year on year) and this helps keep inflation down globally. The strong Chinese currency helps countries that have seen their currencies weaken as it makes them more competitive in exports. FIIs too will prefer countries where currency is cheap rather than expensive.

On the negative side, a weak Chinese economy will pull down the economies of many countries, including Japan and other South-East Asian countries, that have high trade linkages with China. A weak Chinese economy can pull down global growth and this can lead to a self-fulfilling cycle of falling growth.

The markets are suggesting that a weak Chinese economy is helping other economies and hence the difference in performance. This trend could continue until China gets back on its feet.

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

{kind=link}

](https://images.firstpost.com/wp-content/uploads/2012/08/china_currency2.jpg){kind=link}