"Post office, PPF rates set to rise, but not by too much")

By R Jagannathan

For a finance ministry that has been advising the Reserve Bank of India (RBI) to think “out-of-the-box” on interest rates, here’s a reality check on double-standards: faced with a sharp drop in collections under post office savings schemes, it may end up recommending a hike in interest rates.

Data for April-June 2011-12 show a Rs 26,500 crore decline in postal savings collections compared to a rise of Rs 13,250 crore in the year before. The finance ministry has used this number to argue two things: one, that it now needs to borrow more from the market since small savings collections are falling, and two, it must raise interest rates on small savings.

The first argument, of course, is specious, since 80 percent of small savings collections go to the states. If collections have fallen, the centre’s loss is only 20 percent of the drop - or just about Rs 5,300 crore out of the total drop of Rs 26,500 crore.

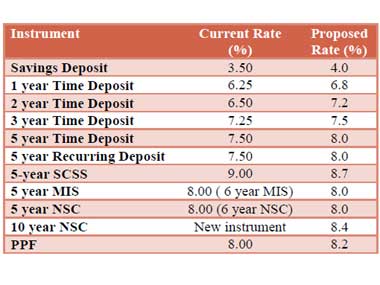

[caption id=“attachment_103306” align=“alignleft” width=“380” caption=“Data for April-June 2011-12 show a Rs 26,500 crore decline in postal savings collections compared to a rise of Rs 13,250 crore in the year before. Pawan Kumar/Reuters”]

[/caption]

[/caption]

On 30 September, the finance minister announced a whopping Rs 53,000 crore additional borrowing programme this year - and, clearly, this magnitude has little to do with the small savings decline.

So let’s be clear: postal savings rates have to be raised for the same reason banks are raising rates - to give depositors a better deal when inflation is still roaring.

Little wonder, The Times of India now informs us that Pranab Mukherjee’s ministry will be proposing a rate increase in post office schemes and even the tax-free public provident fund (PPF).

Post office rates range from 3.5 percent to 8 percent, with 9 percent being paid on the Senior Citizens’ Savings Scheme. All schemes effectively earn zero or negative rates of return after inflation, barring possibly the PPF and National Savings Certificates (NSCs), which yield more than 8 percent due to tax benefits under Section 80 C of the Income Tax Act.

The upshot is that small savers are sure to get better rates shortly. The new rates, recommended by the Shyamala Gopinath Committee on a Comprehensive Review of the National Small Savings Fund (NSSF), are basically about benchmarking postal savings rates to the prices of government securities.

If the recommendations are accepted in toto, the basic savings deposit rate for 2011-12 will rise to 4 percent from 3.5 percent to align the rate with the bank savings rate. Time deposits will be higher by 0.25-0.55 percent, with PPF getting 8.2 percent ( See chart ).

{kind=link}

The Gopinath Committee also called for the creation of a new 10-year National Savings Certificate with 8.4 percent interest, but the bad news for senior citizens is that it would have cut the top rate for them to 8.7 percent from the current 9 percent. However, given the political sensitivity of the senior citizens’ rate, and given the fact that banks already offer more, it is unlikely that the finance ministry will accept this part of the Gopinath report.

The Times of India report also says that Kisan Vikas Patras (KVP), whose abolition was sought by the Gopinath committee on account of its money-laundering potential, may be retained on the ground that it is a largely rural instrument.

The key point, however, is that the government’s huge resources gap is forcing it to raise interest rates on small savings.

The Business Blog is a daily business blog anchored by Firstpost senior editors. It will offer quick comments and insights into major business news developments from the pink press.