"Follow these thumb rules to live life free from financial stress")

ByRanjeet S Mudholkar

Financial Planning is a goal based approach to investing which ensures that all the financial goals of an individual are met by planning during the working life of an individual. It envisages identification of goals and making strategies and implementing them to meet the goals in consultation with a financial adviser. However there are certain ground principles or thumb rules which, if followed can ensure that one leads a life which is free from anxiety on financial front.

The genesis lies in the bifurcation of income into Expenses, Debt Servicing and Investment to attain future goals. There are four major areas in which income could be bifurcated:

1. Taxes

2. Expenses

3. Debt Repayments

4. Investment for the attainment of financial goals.

Taxes are mandatorily paid after rationalising of tax liability by tax planning ,once the taxes are paid, the net in hand income of the individual needs to be bifurcated in such a way that there is no scope for financial anxiety. If one is able to ensure that out of the net after tax income of an individual, not more than 1/3rd goes towards expenses, while 1/3rd is allocated towards debt repayments and the remaining 1/3rd is invested for the attainment of future financial goals, there is all likelihood that all the financial goals of the individual are met and all the current expenses are taken care of.

If followed, the above rule shall ensure that one is never short of money at the crucial times in his life as well as all the mortgage payments are taken care of along with the future financial goals.

[caption id=“attachment_1081103” align=“alignright” width=“380”]  Getty Images[/caption]

Within the limits of 1/3rd under each head certain discipline needs to be maintained :

(i) Under the head of debt out of 1/3rd portion of the income, 2/3rd of one third amount could be used towards housing loan EMI while the rest could be utilised toward creation of other assets.

(ii) Under the head of investment 1/3rd could be allocated to Equity and Mutual funds, 1/3rd to be allocated gold and inflation related investment while the remaining 1/3rd could be allocated to liquid and debt instruments. This would ensure that the effect of diversification is built in the portfolio with a reasonable return.

(iii) Under Expenses head, the expenses could be divided under the heads of discretionary, non discretionary and occasional expenditure like festival, functions and ceremonies in 1/3rd proportion each. Non discretionary expenditure includes the expenses on which there is no control of an individual and they are to be undertaken irrespective of the level of income for e.g. expense on groceries while discretionary expenses are the ones which could be avoided /curtailed. It is advisable that one makes a corpus for occasional expenditure by investing the amount equivalent to 1/3rd of the amount allocated to the head of expenses. This is recommended as the occasional expenses are less in frequency and more in quantum. Even for discretionary expenses one should make a corpus of 1/3rd amount so that the discretionary expenses can be undertaken in lump sum after proper analysis.

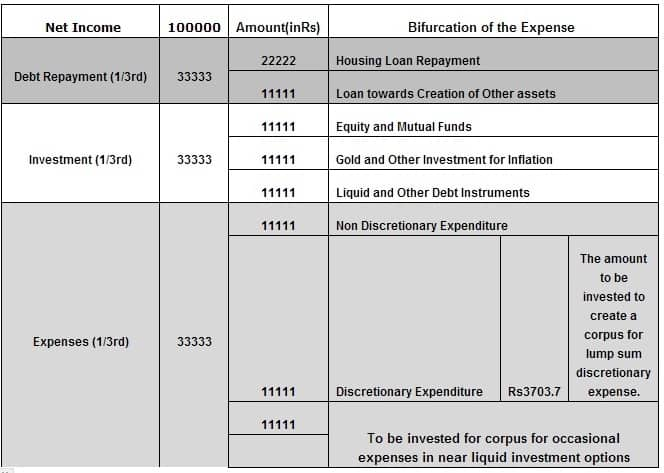

As an example, take a case of an individual having a post tax income of Rs 1 lakh per month. Following is the prescribed distribution of the income as per the rule. (See table here.)

If the income is distributed as per the distribution displayed in the table above then all the financial goals of the said individual would be met along with maintaining current life style with the creation of assets for the future use.

Additionally it must be ensured that debt must never be taken for expenses and should also be avoided for depreciable assets as it results in erosion in net worth.

In addition individuals may seek tax benefits from Investment in certain financial instruments that is allowed as deduction from taxable income under section 80 C of the Indian Income Tax Act, 1961 and the interest on housing loan is deductible from the taxable income under section 24 of the same Act up to a limit of Rs 150,000 in a year for self occupied property while there is no limit for if the property is lent out. Thus it must also be ensured that the distribution in the heads mentioned should be done in a tax efficient manner which can maximise the in hand income of the individual which could further be used either for current consumption or planning for the future.

At the same time, while selecting the investment products or looking for the right loans within the limits as mentioned above, it is beneficial to take the services of an expert like a CertifiedFinancial Planner (CFP) professional who is equipped to guide in the related areas.

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

](https://images.firstpost.com/wp-content/uploads/2013/08/tax350.jpg){kind=link}

{kind=link}