"Can't pay your bills? Here's how you can avoid the dreaded debt trap")

By: Ranjeet S Mudholkar

Financial Planning is an approach which ensures that one leads a life free from financial worries.

It involves goal-based management of one’s finances. The goals could include saving for retirement, buying a house or an exotic vacation abroad. In today’s scenario debt is easily available for an earning individual. The easy availability of loans has led to unwarranted consumerism which is not typical to Indian mindset.

To ensure financial well being, it becomes very important that the debt repayment capacity of an individual is suitably determined. It calls for effective management of debt in today’s scenario if one wants to lead a life that is free from financial worries.

While there are many factors which go in determining the debt repayment capacity of an individual, the following principles of Financial Planning shall ensure that one is not overburdened with debt and at the same time not underutilising the leverage that debt can provide towards creation of assets:

1. Net after tax Income of an individual should be divided in three parts, wherein 1/3rd should be used for current expenses, 1/3rd should be used for debt repayment and 1/3rd should be used for investment for the future.

2. Debt should not be taken for acquiring a depreciating asset. An example could be buying a mobile phone or white goods on loan.

3. There should be a limit on the expenditure which does not have salvage value e.g. holidays, entertainment etc

[caption id=“attachment_1094387” align=“alignleft” width=“380”]  AFP[/caption]

As an example of rule number one if an individual has a net take home salary of Rs 12 lakh per annum then he should ideally be contracting a home loan not exceeding Rs 30 lakh for a 10 year term at 10 percent rate of interest.

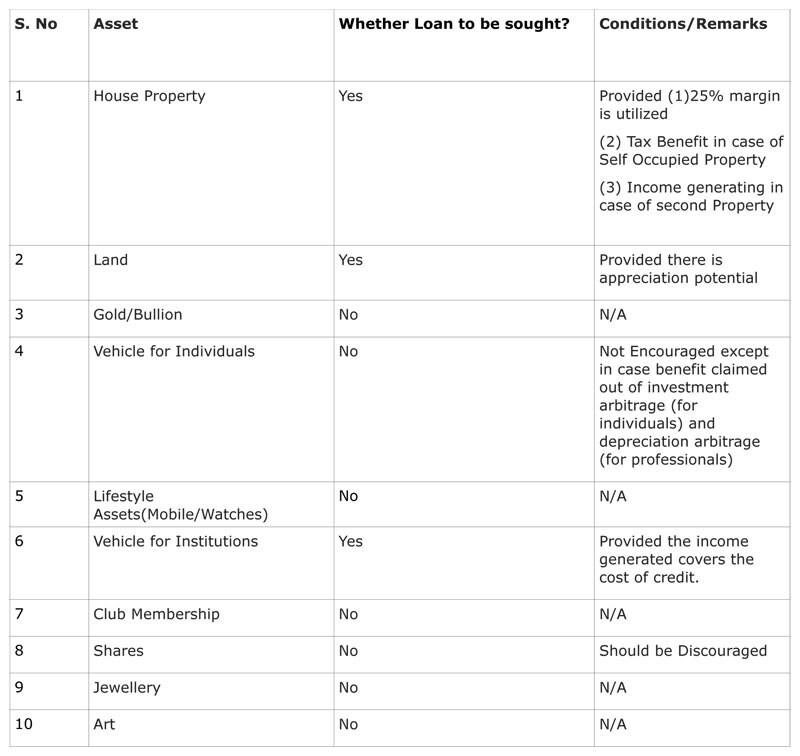

The relevance of the second rule lies in the fact that the debt taken in an appreciable asset like house property increases the net worth of an individual, while debt taken for a depreciating asset like a mobile phone or laptop will reduce the net worth of the individual.

This Table ( view here )gives an indicative list of Assets and suggestion w.r.t. procurement through loan.

Furthermore, debt should be preferably taken in areas where it can provide tax advantage.

Housing is one such area where interest paid gives leverage for the housing loan taken. Under section 24 of Indian Income Tax Act, 1961 interest paid on the housing loan is allowed as a deduction from the taxable income for a self occupied property and there is no such limit if the property is let out. In addition the principal repayment during the same can be deducted up to a limit of Rs 1 lakh in the year under section 80 C of the act. In the Union Budget 2013-14, government has given an additional limit of Rs 1 lakh for first time home buyers in the interest repayment for the current year under Section 80 EE provided certain specified conditions are met.

In addition to the principles mentioned above, instruments like credit cards which offer rolling credit should be used prudently. While there is no harm in using a credit card, if one repays within the stipulated time limit, the payments outside the time limit attract huge interest charges. On an average one takes more than 6 years to repay the total credit card outstanding if one keeps on paying minimum balance paying nearly 2.5 times the original borrowed amount.

Undue borrowing with the instruments such as credit cards or personal loans may lead to a situation where one is forced to compromise on one or more of his/her financial goals. One should avoid getting into a situation of debt trap where the income/savings of an individual are inadequate for debt repayment and one has to acquire new debt to make good the obligations of the previously taken debt.

Debt should be used constructively where innovative products like Margin Funding can help provide leverage which may result in higher returns. Products like reverse mortgage can be used very efficiently by individuals for retirement planning.

Debt can provide leverage for creation of assets and higher returns if used prudently in consultation with an expert like a Certified Financial Planner (CFP) professional or else one could fall into a debt trap.

Ranjeet S Mudholkar, is Vice Chairman and Chief Executive Officer, Financial Planning Standards Board India (FPSB India). The views expressed here are personal, and do not necessarily represent that of the organization

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

](https://images.firstpost.com/wp-content/uploads/2013/09/creditcard-afp.jpg){kind=link}

{kind=link}