"Buy or rent a home? Read this and take a call on affordability")

By Ranjeet S Mudholkar

To decide on a home, and that too whether to rent a place or buy a home is the most important financial decision one has to make. Broadly there are two categories of factors that are needed to be considered

a. Financial aspects of the decision

b. Personal and emotional aspects of the decision.

Financial Aspects:

Looking at the financial aspects following are the steps one needs to take:

Evaluating Current Finances

The first step in the decision making process is whether or not one can afford to purchase a house. Issues to consider include one’s ability to make down payment and other upfront charges like brokerages and taxes. These costs would be substantially more than the initial security deposit one would have to pay in case of renting a house.

Even if one has the money to make the initial payments in the purchase of the house, the battle is still half won.

One still needs to consider the ongoing expenses once he/she starts living in the house. There are various estimates as to what part of the net income of the individual should go for debt repayment, but broadly adopting a 1/3rd approach which says that out of the net in hand income of an individual not more than one third should go towards debt repayment while out of the remaining, 1/3rd could be used for expenses with the remaining 1/3rd to be for investment. This can act as a thumb rule while deciding the affordability of the house.

As an example, an individual with a post tax salary of Rs 9 lakh should pay a maximum of Rs 3 lakh in the form of debt repayment, which makes his monthly repaying capacity as Rs 25,000. This would make him eligible for a loan of Rs 25 lakh (at 8% for 20 years) and taking 80% Loan To Value ratio, he/she would be in a position to buy a house costing Rs 32-33 lakh.

However, if one finds himself/herself able to make initial payments and service the ongoing debt, there are other factors that need to be considered. In a city like Mumbai a rented apartment in suburbs or the main city would cost considerably lower on a monthly basis then the estimated mortgage payment on the same period. Moreover, you should not forget the maintenance cost that if you have to pay in case of a purchased house.

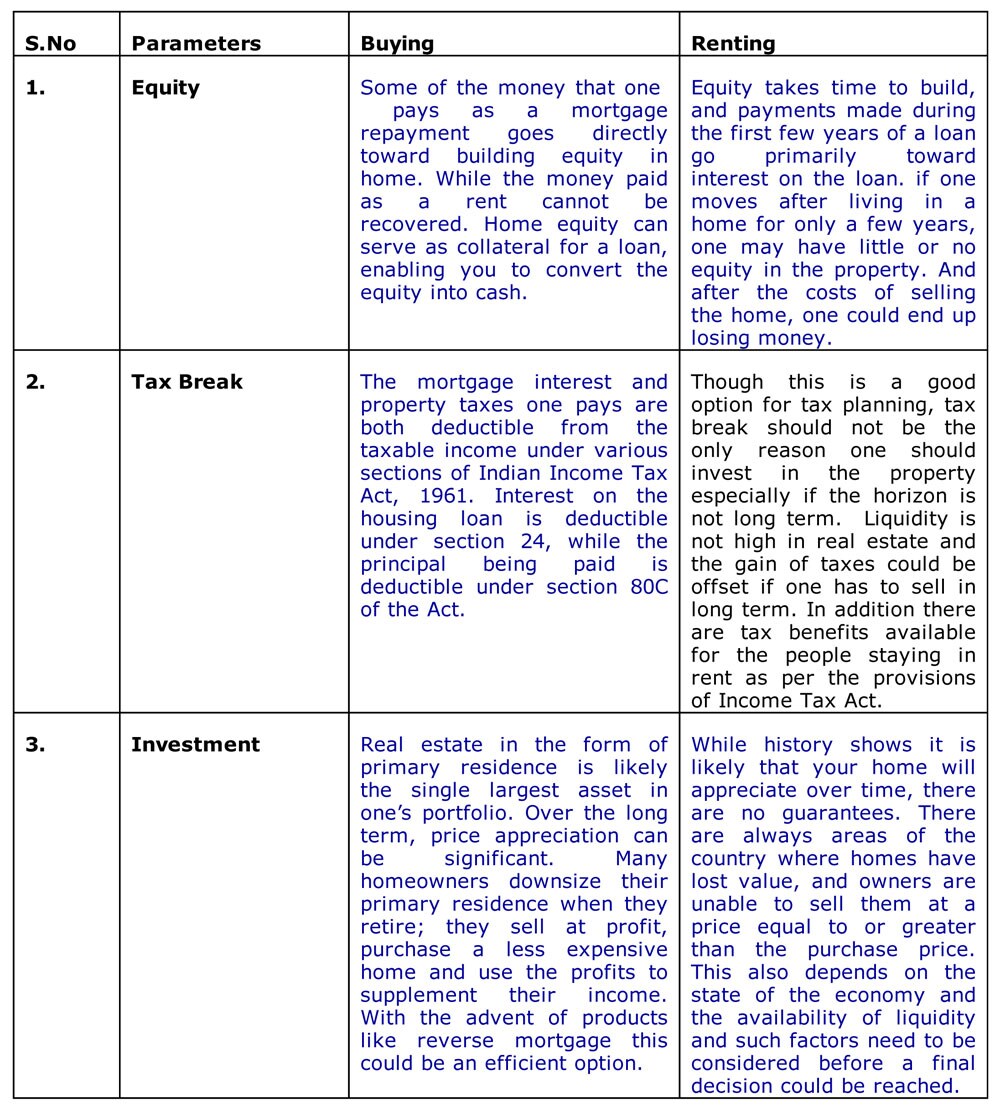

Long Term Cost/Benefit analysis

Proponents of buying often cite the ability to build equity, the tax breaks and the investment value of a home as solid reasons to buy instead of rent. While these arguments have merit, there are downsides to all of them. This table ( click here ) outlines the positive and negative long-term realities of the equity, tax breaks and investment value associated with buying a home.

The number of years one has to live in the house is an important determinant of the decision of buying versus renting.

[caption id=“attachment_1111449” align=“alignleft” width=“380”]  The number of years one has to live in the house is an important determinant of the decision of buying versus renting.[/caption]

In addition to the financial factors mentioned above there are emotional factors and personal preferences that goes into one choosing a place to live. These could be enumerated as follows

a. Amenities

Renting generally provides more amenities than buying for the same amount of money spent. Upscale apartment buildings in every city provide facilities like swimming pool, gymnasium and parks at a comparatively lower monthly rent than a mortgage for a property with the same attributes. On the other side of coin, there are affordable homes with private outdoor spaces that one can customize to liking.

b. Flexibility

Renting a place gives you significantly more freedom to leave at a moment’s notice. The financial consequences of breaking a lease are minimal and can be addressed by paying up. Homeowners wanting to leave their current residence face a much more complicated process while selling their property. The installment still needs to be paid and the maintenance needs to be taken care of while one is waiting to find a buyer.

Unless money is no object, the transition to a new place of residence is likely to take months, not days. On the other hand, with the flexibility of renting comes also some instability. The landlord can always raise the rent or ask one to move before one is ready to do so.

c. Environment

The environment one chooses to live plays a very important role in the quality of life. The accessibility of shops, the quality of life, the modes of travel and the neighborhood have the potential to impact your living environment. If one can afford only those properties in environments that do not fit his/her preferences, one needs to think about whether he is willing to forgo these preferences for the sake of owning a place.

d. Emotional Satisfaction

Homeownership is often the dream of an individual. There’s just something emotionally appealing about putting down roots, getting involved in the community and having a place to call one’s own. Of course, homeowners also need to worry about the long-term character of the neighborhood and keep up with maintenance in order to sustain property values. If the house is required to spend the time between the coming and going to work renting may be more appropriate with the worries of maintenance with somebody else.

The emotional and preferential factors mentioned above cannot be calculated in mathematical terms but they have a lot of value in ensuring that one gets a peaceful life. If one has the financial capacity to do both; to pay the rent and make mortgage loan payment then one may chose any one over the other.

In conclusion it can be said that buying a home is an important decision of one’s life and should be considered for some time in consultation of an expert like a Certified Financial Planner (CFP) professional who will ensure that the decision is in consonance with the other financial goals as enumerated in your financial plan.

Ranjeet S Mudholkar, is Vice Chairman and Chief Executive Officer, Financial Planning Standards Board India (FPSB India). The views expressed here are personal, and do not necessarily represent that of the organization.

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

{kind=link}

](https://images.firstpost.com/wp-content/uploads/2013/09/property.jpg){kind=link}