"A step by step long term financial plan for newly weds")

by Ranjeet Mudholkar

Marriage is an important decision in life and is a major juncture when two individuals come together and chart out their common goals in life. This also heralds a crucial life stage where the risk profile of family as a unit as well as their lifestyle undergoes a substantial change. Marriage marks a change from one phase of life to another where most of the parameters of financial decision making undergo a change. It is expected that India shall witness over 200 million marriages in next two decades. This coupled with growing level of education and urbanisation in nuclear family mode would lead to millions of young couples requiring systematic management of their finances.

The new life begins with togetherness in all aspects and financial transactions are no different. The decisions which were individual hitherto become combined as the stake holders increase resulting in change in decision parameters. Though the priorities are different at young ages, rationality needs to be exercised in the decisions which have a potential financial impact. Engaging an expert is warranted at this stage that may help the couple in the crystallization of the financial goals.

There may be two situations in case of young couples

1. Both are working

2. One is working

[caption id=“attachment_868427” align=“alignright” width=“380”]  Reuters[/caption]

In both the scenarios the planning aspects of a young couple may vary from starting a family immediately to postponing the same till stability is reached in job, either individual or jointly. In some cases a basic set up such as a house of one’s own is prioritised. In addition to the necessities, the inclination is more towards spending on leisure such as frequent, extended holidays and lifestyle. There may be a tendency to spend more on leisure and luxury and even borrow for the same.

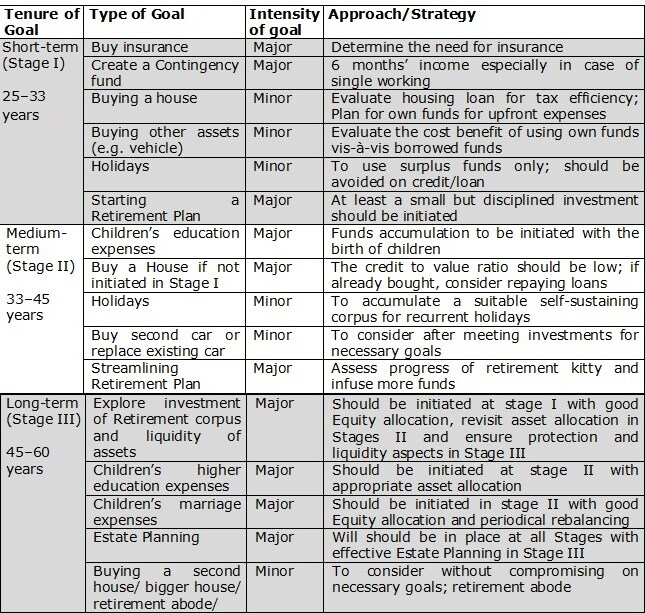

The table below summarizes a young (both or single working) couple’s immediate, medium and long-term goals with suggested strategies from the viewpoint of a professional Financial Planner. (See table here)

Financial Planning is a dynamic discipline in a way that no two individuals can have all the goals same, and the tenure and manner of their achievement. A thumb rule in this respect is ideally set aside 1/3rd of income for household expenses, the other 1/3rd on loan servicing, while routing the balance 1/3rd to investment vehicles to achieve one’s financial goals. It may happen that this ratio in short phases is not maintained, but reverting to this principle would always infuse the required discipline.

If both are working, then buying a house could be very helpful in tax planning as both of them are individually eligible for a deduction of taxable income up to a limit of Rs 150,000 per annum on the interest paid towards the housing loan and principal is deductible up to a limit of Rs 1 lakh per annum as per the Sections 24 and 80 C of Income Tax Act 1961, respectively. In case only one is working this benefit is available to the working member only and other provisions like clubbing of income needs to be taken into account while calculating the tax liability for the year.

Financial transactions and documents may also be managed jointly and it needs to be ensured that proper nominations are in place for all the investments and bank accounts and the other one is clearly aware about the investments made and insurance policies taken so that there is no inconvenience in case of any eventuality.

Joint bank accounts could be opened with husband being primary signatory in one and wife being in another.

Marriage is an ideal stage and event when one can take the stock of financial situation and set up the financial goals of the family. As can be seen from the above illustration, a financial discipline exercised in stage I, sets the theme of well being in the subsequent stages. In stage II, the household expenses are on the rise due to education of the children and incidental expenses thereto however, the same should also be provided for in Stage I itself. The long-term wealth creation should mark the planning immediately after marriage.

It is advisable to approach a professional financial planner for charting out one’s Financial Plan. The assistance of a Certified Financial Planner or CFP professional would be helpful in setting up the priorities and evaluating the needs of a young couple. It can help to develop a robust financial plan, which would be reviewed periodically thereafter to fix the inconsistencies, if any.

Ranjeet S Mudholkar, is Vice Chairman and Chief Executive Officer, Financial Planning Standards Board India (FPSB India). The views expressed here are personal, and do not necessarily represent that of the organization.

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

{kind=link}