"Six reasons why 7.6% GDP growth estimate for FY16 is a myth")

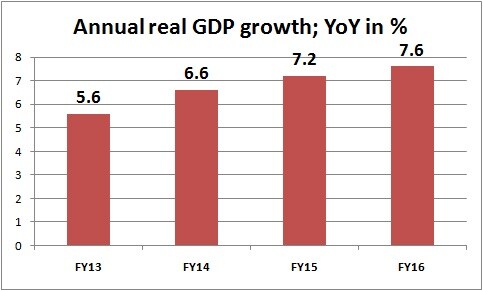

The gross domestic product (GDP) numbers for the third quarter, at 7.3 per cent, and the advanced estimate for fiscal year 2016, at 7.6 per cent, has enthused the Narendra Modi camp. At this rate of growth, India retains the tag of the fastest growing major economy in the world, beating China (whose economy, by the way, is five times larger than that of India). The huge upside on the manufacturing growth in the Q3 numbers has surprised all economists. The manufacturing sector (including electricity and mining), grew at over 11.03 per cent, whereas Index of Industrial Production (IIP), core sector growth and PMI not necessarily show such a pick-up.  The numbers give room for chest-thumping for the BJP camp, since the full year estimate is higher compared with the 7-7.5 percent growth estimated in the mid-year economic review (even though it is far lower than 8-8.5 percent estimated earlier). To be sure, directionally, economic growth scenario is looking positive but the levels of growth registered across certain segments, such as manufacturing, warrants caution. There are a few aspects that needs to be looked at closely and possibly owes an explanation from the CSO: For one, how does one explain the manufacturing segment sharply growing by 11.03 per cent in the third quarter, during which the industrial output numbers, core sector growth and corporate sector performance, have languished? This number is clearly out of sync with other related indicators. A good part of the (about 69 per cent) manufacturing growth has been generated using the data from the corporate sector (data provided by Sebi) and rest from IIP. But, the question is how real this growth is when data from the Ministry of Corporate Affairs (MCA) is not taken into account yet. Also, in Q3, the whole of corporate sector data is not yet available.  There has not been any marked improvement in the corporate earnings so far. The value added component has increased (on account of lower commodity prices and lower interest costs) but the output hasn’t. This trend cannot sustain for long. Second, if one discounts the sharp, unconvincing, jump in the manufacturing segment and looks at the internals of GDP numbers, growth has largely happened due to urban consumption, whereas rural growth, exports (which have fallen for 13 consecutive months) and fresh capital investments (as shown in the gross fixed capital formation numbers that fell to 27.8 per cent of GDP from 30.5 per cent in Q2 and 30.9 per cent in Q1) have fared poorly. “Clearly the CSO needs to explain why manufacturing sector growth is on the higher side when data is essentially telling us otherwise,” said Gaurav Kapur, economist at RBS bank. The point is at this juncture, urban consumption is the only factor that is convincingly holding the growth, not manufacturing. As Firstpost highlighted before, going ahead, the economy will likely derive strength more from the consumption side than investments, especially when the government intends to put more money into the hands of the people by way of 7th Pay Commission, OROP and employment guarantee schemes. Thirdly, agriculture is a puzzle. If the economy has to grow at 7.6 percent for the full year, as the advance estimate suggests, this sector has to grow at least 2.6 per cent in the fourth quarter. In the third quarter, this sector posted a contraction of negative 1 percent. It is almost impossible to achieve that kind of growth in the fourth quarter even if one takes into account the base effect of last year as cultivation has suffered on account of uneven distribution of rains. Already, the Rabi sowing is registered down by 25 percent this year. Fourthly, some economists, such as Ritika Mankar Mukherjee of Ambit, have been skeptical on the 7.6 percent growth highlighting the protruding disconnect between the GDP and real situation on the ground. “The new GDP series and the information that it is conveying, not just in terms of levels but also in terms of the direction, seems very counter-intuitive,” said Mukherjee of Ambit. “We maintain our point of view that GDP growth data is being overestimated by the CSO and will eventually be revised downwards as the first, second and third estimates are published,” Mukerjee said. So far, data is no available to compare the GDP growth with that of previous years’. It is even more important for the government to offer back series data for at least 15-20 years without delay to make the new GDP methodology more trustworthy. Fifthly, in a larger context, has the country seen rise in employment and income levels in line with the high economic growth as depicted by the GDP numbers? There is no clear estimate (on account of poor data infrastructure) to see the trend of job generation in the economy. Economists are unsure about this part although there is a general belief that the construction sector has given employment push in recent years. If indeed high growth is not resulting in more jobs, there is something wrong with the way we assess growth of the economy. Sixthly, the government is clearly under pressure to aggressively cut their spending if it needs to meet the fiscal deficit target of 3.9 percent in fiscal year 2016 and 3.5 per cent in fiscal year 2017, which will again put pressure on growth. Given that the nominal growth rate is projected at 8.6 percent and finance minister Arun Jaitley is determined to stick to the fiscal deficit path, cut in spending is necessary, given the poor show on disinvestment. The question then is where will the growth come from in the economy? In short, all this suggests that there will be sharp downward revision of the 7.6 per cent number and the actual growth may settle somewhere around 7.2 percent and 7.4 percent. According to economists, if one takes into account the deceleration in manufacturing growth in the third quarter, the October-December quarter growth should have been around 6.8 percent. It is logical that when the new methodology setting in, it will take time to stabilise but the sharp revisions (Q1 GDP figure was revised upwards to 7.6 percent from 7.0 per cent) and the fiscal 2015 number revised downwards to 7.2 per cent from 7.4 per cent) in the past warrants caution. Kishor Kadam contributed to this story

The manufacturing sector (including electricity and mining), grew at over 11.03 per cent, whereas Index of Industrial Production (IIP), core sector growth and PMI not necessarily show such a pick up.

Advertisement

End of Article

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

](https://images.firstpost.com/wp-content/uploads/2016/02/GDP_380.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2016/02/annual-GDP1.jpg){kind=link}