"Check out India's first all-women bank, and it isn't govt's Mahila Bank")

In November last year, the Indian government launched what it said was the first all-women bank in India, the Bharatiya Mahila Bank. That’s what they and most of the mainstreammedia would have you believe. But right before its launch, India’s Finance MinisterP. Chidambaram, known to be a stickler for facts and figures over showboating, ceded that this in fact wouldn’t be the first, but the second bank of this kind.

In 1995, a group of 17 women in Maharashtra’s Satara district had applied for a banking license to open a co-operative bank. The share capital required to set up a bank of this kind was Rs 6 lakh, which was raised up by only women, who bought shares worth Rs 25 each.

The women behind this bank were from small villages in the district and uneducated. Instead of their signatures, it is said that they submitted their application to the Reserve Bank of India (RBI) with thumb impressions. Predictably, the RBI rejected their plea-the women wereuneducated and could therefore not be given a licence to run a bank, it said. But Chetna Vijay Sinha was not one to give up at the first sign of red tape. Encouraged to start the bank after a woman in her husband’s village told her how she wanted an account to deposit small amounts towards a home, Sinha, a former college professor, decided to do somethingabout it. She spent five months giving the women literacy classes. The women reapplied for the licence but were again faced by a new set of challenges. What finally worked was a meeting with the officers at RBI, where the women challenged that they could calculate finances faster than them. This, and a reassurance that the bank will be profitable in a fixed time-frame led to this group of 17 women getting a banking licence.

Making good

Mann Deshi Mahila (Sahakari) Bank finally came into being in 1997, with a primary goal of filling the gap that existed between commercial banks and rural woman. “Back then, opening accounts for those who wanted to save very small amounts was not viable for banks…theywere being refused,” says Sinha, founder and chairperson at Mann Deshi Mahila Bank, pointing out that the bank’s average monthly saving deposit is Rs 75 .

“Women had this problem where family members and husbands would take the money they earned. It was important for them to find some other way to save,” she adds. The bank Sinha envisioned would solve that problem and focus on creating banking products suited to theneeds of women. To ensure that the bank took off the ground and moved towards being a fully operational and profitable one, she built partnerships with organizations like German government-backed GIZ and Deutsche Bank since 2010.

The first hurdle Sinha foresaw was getting the women to know what the bank could do for them. But in rural India, reach is more than setting up branches and ATMs. Since it wasn’t possible for many of the women to go to the bank and learn what was being offered to them, doorstep banking was introduced early on, with female agents going door-to-door to takedeposits. Today, with handheld devices, these agents make real-time transactions, including giving out micro-loans to women for personal emergencies and to help them set up micro-enterprises.

Vanita Pise, Chief Administrative Officer at Mann Deshi Mahila Bank says “rural women think that taking a loan is a burden. Taking a loan of a small amount encourages them and they are able to add value to whatever businesses they have started.” Pise herself was a customerof the bank. She tells us how she took a loan of Rs 5000 for rearing buffaloes. After repaying that loan, she took another loan worth Rs 10,000 to start a micro-enterprisebuying a machine that makes paper cups.

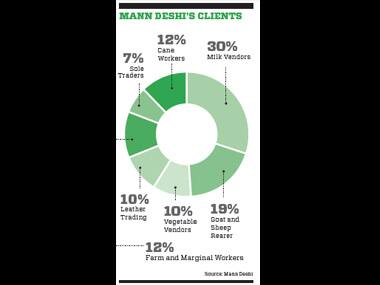

In 2006, Pise got the Women Exemplar Award from the Confederation of Indian Industries (CII). “This [Pise’s recognition] encouraged other women to come forward,” Sinha says. Today, the bank reaches out to about 2.18 lakh women in rural Maharashtra through its 300 agents and eight branches. Its service offering has also expanded to include insuranceproducts and pension schemes. The bank currently has deposits worth Rs 57 crore and advances worth Rs 39 crore. True to its promise to the RBI, the bank has been profitable since 2001 and made a profit of over Rs 50 lakh in FY13.

More products

In 2006, Mann Deshi also set up a business school for rural women through its foundation that works with the rural women on business literacy programs. The courses range from three days to 45 days, Sinha informs. It also runs a mobile business school that travels to remotevillages to impart business training to rural women.

The foundation also runs a community radio station and helps women understand their property rights. The organization has also set up a Chamber of Commerce for rural women entrepreneursand runs a 24 hour helpline. According to Sinha, the bank has been growing at an annual rate of 30 percent.

The bank is also a consulting partner for a finance company that was bought by a group of investors in 2012 to provide loans in other states. The bank is looking to expand to Jharkhand and Bihar by next year, she says, adding, “the aim is to help a million women micro-entrepreneurs by 2020.”

Last month, Sinha was identified as Social Entrepreneur of the Year by the Schwab Foundation for Social Entrepreneurship, a sister organization of the World Economic Forum, in partnership with the Jubilant Bhartia Foundation. Shyam S. Bhartia, Director at JubilantBhartia Foundation, says that Sinha and Mann Deshi Mahila Bank ticked the right boxes when it came to innovation, sustainability, direct social impact, reach and scope and replicability.

What worked in Sinha and the bank’s favor, it is said, are the doorstep banking initiative along with its other customized products designed specifically for the people of the region like-a zero percent interest bicycle loan for young girls to encourage them to go to school. More such products, says Sinha, are on the way as the bank expands its geographic reachwithin India.

This article appeared in Entrepreneur India magazine.