"SBI shows promise, but Dena, OBC feel bad loan heat; what is in store for state-run banks")

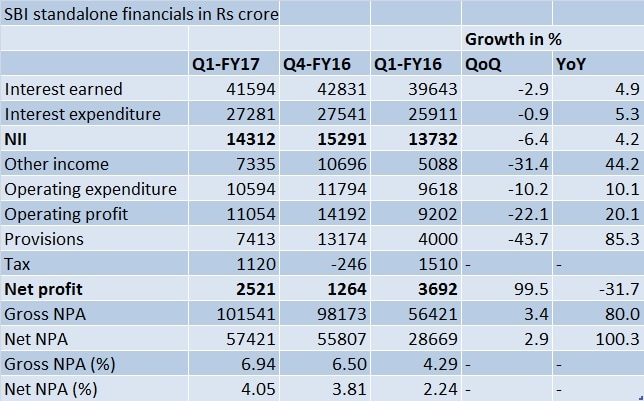

How bad is the bad loan problem in the banking sector? The April-June numbers of State Bank of India (SBI), released on Friday, shows that despite a slight increase in the gross non-performing asset (GNPA) numbers (from 6.5 percent in the March-quarter to 6.94 percent in the June-quarter) SBI hasn’t disappointed the market. [caption id=“attachment_2772680” align=“alignleft” width=“380”]  Reuters[/caption] But even then, SBI’s earnings have been hit by sticky assets. Its net profit dropped by 31.7 per cent, year-on-year, hit by provisions worth Rs 6,340 crore on the bad loans, higher than Rs 3,360 crore in the previous year. Under norms, every bank needs to set aside money against bad loans. Depending on the classification of the asset, the provision amount can differ. SBI is an exception. When it comes to other state-run banks, the pain continues to be severe. For instance, Oriental Bank of Commerce, the bad loans have almost doubled to 11.45 percent of total loans as at end-June, as compared with 9.57 percent in the preceding quarter. Dena Bank too have posted earnings battered with sticky assets with its Gross NPAs rising to 11.88 per cent in the June quarter compared with 9.98 percent in the preceding quarter. The picture is worse with certain other lenders like Indian Overseas Bank (IOB) which is almost on the verge of a crisis with its gross bad loans touching over 20 percent. At the end of the June quarter, the total gross non-performing assets (GNPAs) of the lender have touched a record high of 20.48 percent of its total loan book (of Rs 1,65,556 crore). In other words, one out every five rupees lent by the bank has now gone bad. According to a Firstpost analysis, that’s the highest level of bad loans of IOB in at least 14 years. Total losses of the bank, in the last one year (four quarters put together) stood at Rs 4,467 crore.  The reason for the sharp jump in the NPA level of banks in recent months (since September last year to be specific) can be attributed to the ongoing bad loan clean-up exercise forced on banks by the Reserve Bank of India (RBI) under Raghuram Rajan in September last year. Rajan has given a deadline of March, 2017 for banks to clean up their balance sheets. The exercise has been welcomed by most experts since it has helped to dig out the existing bad loans on the balance sheets of banks for long. Rajan has only forced the banks to state the existing problem upfront instead of postponing it. In total, the gross NPAs of the banking sector is well above Rs 6 lakh crore as at end March. Over 90 percent of these bad loans are on the books of government banks. What is in store for these lenders? The immediate challenge for these banks is funds. They will have to turn to the government to find the capital required to service their balance sheets, meet the Basel-III requirements and expand credit. It also indicates that the government’s current capital infusion programme is too inadequate considering the huge funding gap in the public sector banks. Under the ‘Indradhanush’ revival plan for PSBs, the government plans to infuse Rs 70,000 crore in the four-year period between 2015-16 and 2018-19 in the state-run banks. In the latest round of capital infusion in July, the government infused Rs 22,915 crore in 13 PSBs. But, analysts and rating agencies have cautioned that this money is not sufficient considering the requirement of state-run banks. For instance, rating agency ICRA estimated that the equity capital required by PSBs would be in the range of Rs 40,000-50,000 crore, much higher than that announced by the government this year. Hence, the government will need to increase the fund infusion significantly for 2017-19, Icra said. Another rating agency, Fitch too has said the same. The mounting bad loan is a reminder to the government that its current capital infusion programme is too inadequate considering the huge funding gap in the public sector banks. Analysts expect the pace of growth in bad loans to come down in the approaching months. But that is still some time away. For now, capital remains a big problem. Data contribution by Kishor Kadam

SBI’s earnings have been hit by sticky assets. Its net profit dropped by 31.7 per cent, year-on-year, hit by provisions worth Rs 6,340 crore on the bad loans, higher than Rs 3,360 crore in the previous year

Advertisement

End of Article

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

](https://images.firstpost.com/wp-content/uploads/2016/05/SBIReuters21.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2016/08/SBI-Q1-FY2017-results-table.jpg){kind=link}