Looking at the broader picture, the government’s move to merge SBI’ five associates and BMB with SBI has all the signs of a forced merger.

(Editor’s note: This is an updated version of an earlier article being reproduced in the context of cabinet clearing SBI associates merger with the parent) The elephant in the Indian banking sector is set to grow even bigger, officially. On Wednesday, the Union cabinet approved the merger of five associate banks — State Bank of Bikaner and Jaipur, State Bank of Travancore, State Bank of Patiala, State Bank of Mysore and State Bank of Hyderabad as well as Bharatiya Mahila Bank (BMB) with State Bank of India (SBI). [caption id=“attachment_2772680” align=“alignleft” width=“380”]

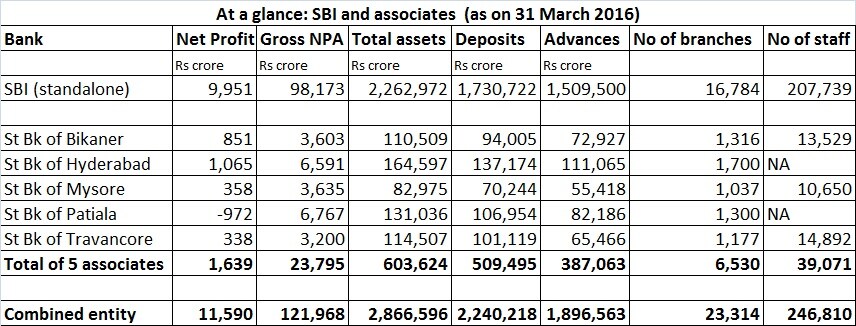

Reuters[/caption] Post the merger, the combined entity will have a total asset size of Rs 28.68 lakh crore as compared with SBI’s standalone asset size of Rs 22.63 lakh crore now. That would also mean the difference between the new SBI and its nearest competitor, ICICI Bank, in terms of assets would be a whopping Rs 21.48 lakh crore. Why this merger now? Looking at the broader angle, the government’s move to merge SBI’ five associates and BMB with SBI has all the signs of a forced merger. Remember, until recently, SBI chairman Arundhati Bhattacharya wasn’t too sure about the merger plan as a priority item on the agenda. This is what Bhattacharya

said in August last year. “I don’t think this is the right time. Because today there are a lot of challenges and those challenges are more immediate than merging banks. The conversion to digital that is happening at such a fast pace, that’s a very big challenge. The fact that we have so many other layers coming in like payments banks, universal banks, licence on tap, disintermediation happening through the crowd funding platforms, crypto currency popping up here and there, so, challenges are multi-fold today,” Bhattacharya said. “Even if I merge them, my balance sheet will not go up, the group balance sheet remains the same. And therefore, the valuation I get will remain almost the same. Only thing that will happen is, I can bring about greater efficiency. But I can do that even without merging,” she said. So what has changed since then to say now that time is right for the grand merger? None of the elements Bhattacharya listed above has suddenly become a non-challenge. They are still around, may be even bigger in nature. So, that leaves us with the assumption that the merger idea has come from the government, the owner of India’s public sector banks (PSBs) including the SBI family. Now, why would the government want SBI to merge all its associates and BMB?

![SBI and associates table - June 15, 2016]()

The only reason could be to create a big-size bank (SBI is the largest in India by assets but not so big if seen globally) that can compete with global banking giants. Bhattacharya told CNBC TV18 in an interview recently that SBI’s total balance sheet size will go up to Rs 37 lakh crore from Rs 28 lakh crore presently post the merger. But, this raises another key question. Is SBI, often dubbed as the elephant among Indian banks, growing too big in relation to its competitors? This is something former RBI governor, D Subbarao had highlighted in August, 2013. “Presently, (there is) significant skewness in the size of banks. The second largest bank in the system is almost one-third the size of the biggest bank. This creates a monopolistic situation,’ Subbarao said. The problem has grown even bigger since then. The concern of policymakers worldwide about the ‘oversized’ financial institutions is justified since if something goes wrong with them, this can have serious ramifications on the whole financial system. This is something that prompted the US federal reserve to finalise a rule in November, 2014 that prohibited any financial company from acquiring another, if the resultant entity’s liabilities exceeded 10 percent of the total liabilities of the financial services system. The rule - Section 622 of the Dodd-Frank Wall Street Reform and Consumer Protection Act - says once a particular entity reaches the specified concentration limit, that bank cannot acquire control of another entity. Logically, the new rule intends to shield the US financial system from the foibles of ’too big to fail’ banks, which could then spark a crisis like the one in 2008 following the collapse of Lehman Brothers, which triggered a global financial meltdown. That meltdown showed that when banks become too big, they can bring down the whole financial system when they lend or invest imprudently. There is no comparison between US and Indian banking systems in terms of size. But, the concerns apply here as well. In July, 2014, the central bank released a framework to identify domestic systemically important banks (D-SIBs) and later classified both SBI and ICICI as systemically important banks. SBI has five remaining subsidiaries - State Bank of Bikaner and Jaipur, State Bank of Travancore, State Bank of Mysore, State Bank of Hyderabad and State Bank of Patiala - of which first three are listed. The bank merged two of its subsidiaries State Bank of Saurashtra and State Bank of Indore during former chairman O P Bhatt’s time, in 2008 and 2010, respectively. In SBI’s case, given the enormous size of the bank compared to its domestic peers, there is an obvious concentration risk that is building up. This is what the RBI has to monitor. If anything goes wrong with SBI, it would have repercussions not only for the bank, but the whole financial system. In a worst case scenario, if a major crisis grips the domestic banking system, a fiscally-constrained government may find it difficult to capitalise SBI, especially if it keeps growing its book at least as fast as the economy. Considering its size and appetite, the elephant is not easy to feed. Yet again, Subbarao’s caution assumes importance. “We don’t need monopolies, instead we need four-five banks of big size, as large banks can become too-big-to-fail, leading to moral hazard problems.” Capital to feed bigger state-run banks is another concern. Already, a rapid growth in bad loans coupled with higher capital requirements under Basel-III norms, has necessitated for additional capital of Rs 2,50,000 crore by 2019. Of the Rs 70,000 crore government planned for PSBs over four years, it has already infused Rs 25,000 crore last fiscal. The government wants PSBs to go the market for the remaining amount. If too-big-to-fail banks meet with a crisis situation, can the government support them is a question. As for BMB is concerned, the idea was a failure form day-1 since creating bank for women and by women assumed that the so-called weaker section would always remain weak and can’t be accommodated in the mainstream. The bottom line is this: As former SBI chairman Bhatt pointed out earlier, it would have made more sense to de-link SBI’s associates with the parent since they are doing good on their own. Letting the elephant grow too big can make it much difficult to control. (Data support from Kishor Kadam)

"SBI-associates merger will create an elephant difficult to tame")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

](https://images.firstpost.com/wp-content/uploads/2016/05/SBIReuters21.jpg){kind=link}