"Narendra Modi has an unenviable task of turning around India’s sagging economy; here are the major challenges new govt faces")

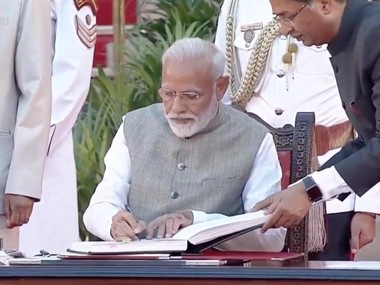

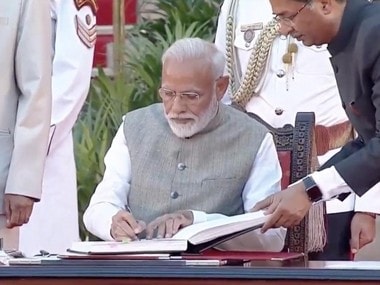

After the Bharatiya Janata Party’s spectacular electoral win, the Narendra Modi-led new government assumed office on 30 May. Investors love stable, majority-led governments that do not need to wait for a coalition’s go-ahead for key reform decisions. From an economic point of view, that is the benefit India has now. What can one expect from Modi 2.0? If one looks at the first term of the Modi government, the economic performance chart gives a mixed picture. On the positive side, the Indian economy has crossed some crucial milestones. Its economic fundamentals improved. Inflation and fiscal deficit figures were brought under control. A very critical piece of banking reform—the Insolvency and Bankruptcy Code, was finally brought to life; the nation embraced a Goods and Services Tax (GST) and social welfare schemes were backed up with the efficient use of a mobile number-Aadhar linked strategy preventing leakages. Jan Dhan accounts, with all its debatable shortcomings, widened the access to far-flung villages where Indian banks typically hesitate to go. The banking sector NPA clean-up initiated in 2015 proved to be a much significant exercise to restore the health of Indian banks for it helped clear the backlog of bad loans that weren’t stated until then. About Rs 9 lakh crore NPAs were added in just three to four years. The balance sheet of banks balance sheets now looks much more reliable. [caption id=“attachment_6729831” align=“alignleft” width=“380”]  Prime Minister Narendra Modi during the oath-taking ceremony at Rahstrapati Bahvan. Twitter@BJP4India[/caption] There were some avoidable economic misadventures too. One such was demonetisation of high-value notes in November 2016 which was intended to kill black money, fake notes, and cash-based corruption. This boomeranged to a large extent with none of the original targets met with in a meaningful manner even though the move triggered a larger shift to e-payment methods. It led to more and more people becoming familiarised with cashless payment products. However, note ban hit the economy hard, shaving off 2 percent from the national gross domestic product (GDP) and breaking the back of an informal economy that relied on cash predominantly. Lack of follow-up on Modi’s much-hyped action plans, for instance, Make in India, impacted its outcome. The government’s reluctance to address land and labour reforms and privatisation of PSUs acted as a huge turn-off for investors. Rising rural distress and unemployment levels in the country were not tackled by the government in its first term. India’s data credibility became a debate even internationally. But one can’t live in the past. The big mandate that has been offered to Narendra Modi in the 17th Lok Sabha elections by Indian voters empower him to undertake the next round of critical reforms in the economy—without coalition pressure—and correct some of the misses in the first term. The large untapped economy, which is now benefitting from lower deficits and inflation, presents a big opportunity for Modi to bring in the next wave of important reforms. Of them, privatisation of weak PSU banks is key. As this writer argued in an earlier article, of the 18 PSUs existing now, most of the lenders have very high NPAs but the balance sheets became more transparent post-the prolonged asset quality review process. This presents an opportunity for Modi to bargain hard with large private investors for an outright sell-off of the government stake in these banks. If the new government doesn’t do it, the gains of PSBs NPA clean-up process will vanish eventually, because their fundamental problems remain. The government holds over 70 percent stake in 16 banks as of end-March, 2019. In at least 12 of them, the government has over 80 percent holding and in six of them, over 90 percent. These are in Andhra Bank, Central Bank, Corporation Bank, Indian Overseas Bank, UCO Bank, and United Bank. Selling this stake will yield significant revenue to government coffers besides freeing up the burden of heavy annual capitalisation in these banks. It is equally important that the government addresses the long-pending land and labour reforms. These are the two main roadblocks to India becoming a global manufacturing hub. An investor looking to set up a shop or factory in India will find it a nightmare to acquire land surpassing a number of clearances at the central and local level. The same is the case with labour laws. Modi will find it tough even now to address politically-sensitive reforms on account of NDA’s insufficient strength in the Upper House. But, with NDA projected to have a majority in another two years, this shouldn’t be too difficult.

Refining the GST structure is key. The multiple slabs/rates and separate rates for individual items, and some technical challenges in the filing of GST needs to be looked into. The country needs to move into a narrow rate structure at the earliest to make the ‘one nation, one rate’ dream true. Presently, the complexity of the GST format makes it a nightmare for businessmen to embrace it with honesty and not engage in tax evasion. Ending the uncertainty on India’s GDP data is critical. The world has begun doubting India’s official numbers on account of a seemingly faulty methodology and lack of a connect with high-frequency indicators on the ground. Ever since the new GDP series was introduced in the early years of Narendra Modi-led government’s first term, there were questions about the accuracy of the GDP numbers. Recently, an NSSO survey confirmed that 36 percent of companies that are part of MCA-21 database of companies and are used in the GDP calculations could not be traced or were wrongly classified. There were also problems with the employment data regarding an NSSO report. The new Modi government must regain the lost data credibility by forming an independent panel to look at data reliability. The new Modi government will have to also renegotiate trade deals and rework strategies for India in the age of an unfolding global trade war. The trade war involving the US, China and Europe will have an impact on emerging markets such as India. There are experts who even term the battle between the big markets as a favourable situation for India where the country can occupy the space of a major manufacturer/exporter to key markets.

Domestically, India is facing a prolonged phase of economic slowdown and demand slump. Vehicle sales have slowed down and FMCG companies are struggling. The government will have to put more money in the pockets of individuals, especially in rural India to revive the demand cycle.

It is even more important now for Modi to tackle the Hinduvta hardline elements in the party and send a clear message to the outside world that his government intends to practice what it preaches—sabka saath, sabka vikas. Investors, in the run-up to 2019 polls, have bet for a stable Modi government rather than a fractured Opposition. With a stable government and strong political leadership, India has a great opportunity to emerge as a major power in Asia and cannot afford unnecessary distractions. (Data support from Kishor Kadam)

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

](https://images.firstpost.com/wp-content/uploads/2019/05/Modi_380.jpg){kind=link}