"Moody’s India sovereign rating upgrade: Old foe has turned friend for Narendra Modi government")

In September 2016, Moody’s Investors Service was not in the good books of the Narendra Modi government. The

finance ministry had then raised a strong objection to the agency’s statement that it was

unlikely to upgrade India’s sovereign ratings anytime soon, ahead of a meeting with finance ministry officials on India’s macro-fundamentals. “The due process has to be followed and you cannot jump the gun, if you are reaching a conclusion before interaction with the finance ministry and the other ministries, then somewhere we see the entire rating process, the methodology, was deficient and that is something we pointed out,” then economic affairs secretary Shaktikanta Das was quoted by Mint, while speaking at the sidelines of a BRICS infrastructure financing conference. “You cannot say that I will give zero weightage and I will wait till infinity to see that these reforms take roots,” Das was quoted as saying. [caption id=“attachment_4214159” align=“alignleft” width=“380”] Representational image. Reuters[/caption] The Modi government had argued that Moody’s must take into account the reforms being undertaken such as GST and bankruptcy code. But, Moody’s maintained that credit implications of reform measures such as GST, bankruptcy code will only become apparent in the medium term. It further highlighted the concerns that weak private investments, slower fiscal consolidation and a high level of bad loans in the banking sector constrain India’s sovereign rating. Just over a year later, Moody’s has returned with good news for the Modi government by

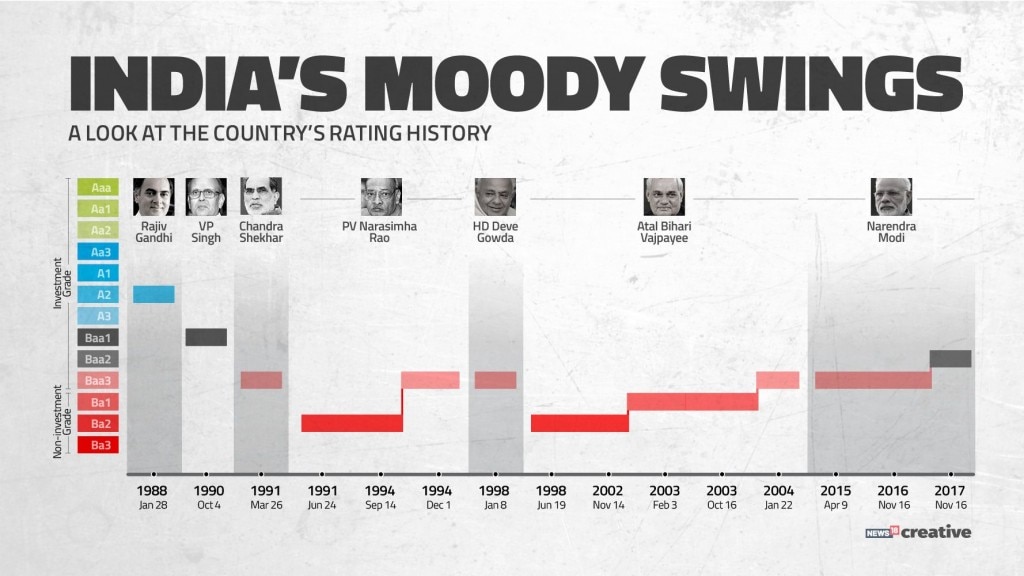

upgrading India’s sovereign rating to by a notch to 'Baa2' , with a stable outlook (Also read:

Full Text: Moody's Investors Service upgrades India's sovereign credit rating to Baa2 ) citing improved growth prospects driven by economic and institutional reforms. An upgrade from Moody’s comes after a gap of 13 years — Moody’s last upgraded India’s rating to ‘Baa3’ in 2004. In 2015, the rating outlook was changed to ‘positive’ from ‘stable’. The rating action is a big thumbs up to the Modi government and comes on the heels of

American think-tank Pew Research Center's report that Modi continues to be the most popular leader in Asia’s third-largest economy of 130 crore people. The rating upgrade particularly mentions the structural reforms being undertaken by the Modi government. “Key elements of the reform program include the recently-introduced GST which will, among other things, promote productivity by removing barriers to interstate trade; improvements to the monetary policy framework; measures to address the overhang of non-performing loans (NPLs) in the banking system; and measures such as demonetisation, the Aadhaar system of biometric accounts and targetted delivery of benefits through the Direct Benefit Transfer (DBT) system intended to reduce informality in the economy,” Moody’s said. This is certainly a big acknowledgement of the reform work committed by the Modi government and, if taken ahead in the desired momentum, can launch the economy on a higher growth path. The other side But, Moody’s doesn’t fail to remind the government about the pending reforms and the concerns in the economic outlook arising from high debt burden. “The high public debt burden remains an important constraint on India’s credit profile relative to peers, notwithstanding the mitigating factors which support fiscal sustainability. That constraint is not expected to diminish rapidly, with low income levels continuing to point to significant development spending needs over the coming years,” Moody’s said.

Similarly, a “material deterioration in fiscal metrics and the outlook for general government fiscal consolidation would put negative pressure on the rating," the agency has warned. Also, the rating could also face downward pressure if the health of the banking system deteriorated significantly or external vulnerability increased sharply, it said. The agency also reminds the government about crucial land and labour market reforms, which, it said, relies to a great extent on cooperation with and between the states. If one briefly revisits the concerns Moody’s highlighted a year ago — weak private investments, slower fiscal consolidation and a high level of bad loans, the first and third factors continue to be painful areas for the government. There has not been any marked improvement in the private investment scenario and banking sector NPA situation. The economy has to revive the private investment momentum and reduce reliance on government spending to push growth in a sustainable manner.

There is a serious problem of not enough jobs being created and beyond recapitalisation, the government has been largely reluctant to go ahead with bold reforms in the banking sector including a clear roadmap to cut government stake in state-run banks. Acquisition of land and labour is still a troublesome area for anyone who wants to set up factories in India. These are important reforms that need to be undertaken.

For now, the Moody’s rating upgrade is big boost for India. With the improvement in the credit profile, it will reduce the borrowing costs of Indian companies and government and, more importantly, help to improve the perceptions of global observers on the Indian economy. The Modi government deserves credit for the reform work it has done, particularly the launch of the GST and reforms in archaic bankruptcy laws.

](https://images.firstpost.com/wp-content/uploads/2017/11/MOODY_RATING.jpg){kind=link}