Unless the livelihood issues are resolved first, there is very little these bank accounts alone can do

If there is one thing Prime Minister Narendra Modi highlights in most of his foreign trips, it is the achievement his government has made with respect to the massive bank account opening drive under his flagship scheme Jan Dhan Yojana. [caption id=“attachment_2718714” align=“alignleft” width=“380”]

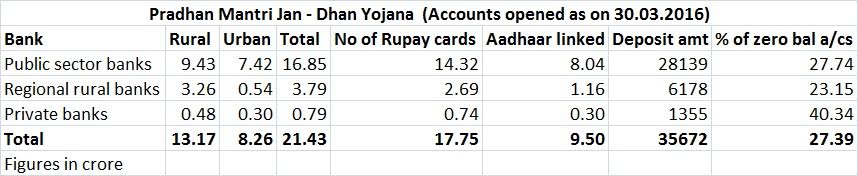

Reuters[/caption] The scheme has, so far, managed to open 21.43 crore accounts, which have mobilised Rs 35,672 crore deposists. Of this, about 9.5 crore accounts have been linked to Aadhaar numbers and 17.75 crore RuPay debit cards have been achieved issued to these account holders. The numbers indeed signify a remarkable achievement, since in the fiscal year prior to the launch of Jan Dhan, India opened just about 6 crore basic service bank accounts (equivalent to the Jan Dhan accounts). But, India’s push on financial push has begun well in the past. A report by British High Commission and Neeti Foundation shows that between 2011 and 2014 the banking account penetration increased in India from 35 percent to 53 percent of population — a period when the UPA was in power. Claims and counter claims India’s push on financial inclusion has been a matter of hot political debate and reason for mud-slinging between the Congress and BJP. In a recent

interview with Firstpost, former finance minister P Chidambaram claimed that Jan Dhan is a repackaged version of the bank account opening drive of the Congress-led UPA government. “I have no objection if they repackage our schemes. Imitation is the best form of flattery,” Chidambaram said. “But, to claim that nothing is done by the previous government is completely wrong. What is Jan Dhan except the same programme we launched under the financial inclusion. We had included by the time we demitted office, as many as 24.3 crore accounts. They simply don’t want to acknowledge this,” said Chidambaram. A major criticism Jan Dhan drive has faced is the issue of duplication when banks were given huge targets by the government within limited period. In March, a

survey by consulting firm MicroSave had warned about the issue of duplication.

![jandhan-table]()

“About thirty-three per cent of the customers indicated that PMJDY was not their first account, in comparison to 14 per cent in Wave-II survey (conducted in July 2015) and Wave-I (conducted in December 2014). Hence, indications are that fresh account opening drives are encouraging clients to open a second account. Most of these accounts are not used,” said the survey. Another survey by World Bank-Gallup Global Findex Survey showed that about 43 percent of the total bank accounts in India are dormant even though bank account penetration has surged in the country in the recent past. The report cited this as a concern for the banking system. However, going by the latest government data, the number of zero-balance accounts has come down significantly since the scheme was launched to 29 per cent from about 45 per cent. Nevertheless, the concern on zero balance accounts has been expressed by Reserve Bank of India (RBI) governor Raghuram Rajan too when he said duplicate accounts would lead to wastage of resources. On Wednesday, former Prime Minister Manmohan Singh too

criticized the progress of Jan Dhan, saying the Modi government has forced banks to open crores of accounts under the Jan Dhan Yojana, which remain unutilised. “All he (Modi) achieved in these two years is forcing crores of people to open bank accounts. But people are asking what will they do with bank accounts when they have nothing to keep in the bank,” he said referring to the Pradhan Mantri Jan Dhan Yojana. But, the BJP’s senior leadership is unfazed with the criticism. Aaadhaar leg-up But, there are no two thoughts on how critical is proliferation of Aadhaar-linked bank accounts in India to ensure that the subsidy rationalisation process is progressing and doesn’t falter half way. As Firstpost pointed out in a

recent article , the passage of The Aadhaar (Target Delivery of Financial and other Subsidies, Benefits and Services) Bill, 2016, in the Lok Sabha assumes crucial importance for the fate of Jan Dhan as it now provides legal backing to identity number. The whole process of subsidy reforms, kicked off during the UPA days and now pushed aggressively by the NDA government, is built on the Direct Benefit Transfer (DBT) channel, based on the unique identity number, or Aadhaar awarded to each citizen. It holds particular importance for the Modi government, and the success of its financial inclusion push under the JAM (Jan Dhan, Aadhaar and Mobile) trinity. For sure, leakage in subsidy has been a grave concern for India’s exchequer for years. Hence, linking bank accounts to a unique social identity number will help plug the spillage. Promise of financial inclusion About 40 percent of Indian population still doesn’t have access to formal banking system. In terms of numbers, the scheme has become an overnight success with its high-speed implementation even bagging a Guinness record. The government achieved this by pushing all government-owned banks to meet the targets. Jan Dhan is arguably the biggest-ever bank account opening drive India has ever witnessed and was designed to offer at least one basic bank accounts to every household, besides access to credit, insurance and pension facilities and offering financial literacy. It also promised RuPay Debit card for every account holder, an inbuilt accident insurance cover of Rs 1 lakh and life insurance cover of Rs 30,000. Besides, the scheme also envisaged channelling all government benefits to the beneficiaries’ accounts. The scope of the scheme was later expanded to offer other products too. Jayanta Sinha, former chief general manager, Rural Banking at SBI, said even before Jan Dhan, KYC norms were relaxed, but lack of financial literacy among the rural population has created problems to expand the reach of banks in the hinterlands. “It is not fair to impose all burden on banks. The government has to take initiative to increase awareness," Sinha said. Even after 65 years of independence and 46 years of bank nationalisation, close to half of India’s population doesn’t have bank accounts. That is despite the country having 27 nationalized banks, 19 private banks, 43 foreign banks and several other layers of banks such as cooperative banks, regional rural banks and local area banks and more recent crop of microfinance institutions. A significant chunk of India’s rural population still depends on private moneylenders to meet their financing needs. Banks have often cited lack of viability in the business model when they operate in the unbanked rural areas. The RBI launched three-year roadmap on financial inclusion in 2010 for banks under which banks were asked to have a board-approved policy on financial inclusion. But the progress has been slow. Prasad P Revdekar, deputy general manager and Thane region head of retail banking at IDBI Bank, said one of the major challenges bankers faced while implementing the Jan Dhan initiative was to convince the customer that there is no free money in these accounts and he has to start transacting in it even to avail the loan overdraft. “Some times, I find customers coming to our bank branches and asking impatiently when he is getting the money in his Jan dhan account. It is so difficult to convince him that there is no free-money in these accounts,” Revdekar said, also adding that there are issues of same person opening multiple accounts with different banks to become eligible for freebies. Over a period of time, such duplicated accounts could emerge as a concern for banking system, Revdekar said. Every zero-balance account cost a bank an average Rs 140 a year to maintain. But Revdekar agrees that Jan Dhan has given the flexibility to banks to significantly relax KYC norms and reach more people in the banking network, where a significant number of tribal population have neither Aadhaar cards nor any other documents to show for KYC proof. Hurried revolution? “Unless the livelihood issues are resolved first, there is very little these bank accounts alone can do,” said Shraddha Shringarpure of NGO Aroehan, which operates in tribal areas of Maharashtra. “Banks have pushed for opening accounts. Hence they have accounts today. But unless their livelihood issues are resolved, they won’t be able to use these accounts much,” Shringarpure said. Nearly 11,000 villages in India are still not connected to the electricity grid and, going by various surveys, at least two-third of rural households still do not have toilets. The question Jan Dhan push raises is this. How far the efforts have progressed in achieving the actual inclusion of India’s poor? This is something the last economic survey too pointed out. “Despite Jan Dhan’s record-breaking feats, basic savings account penetration in most states is still relatively low – 46 per cent on average and above 75 per cent in only 2 states (Madhya Pradesh and Chhattisgarh). Policymakers thus need to be cognisant about exclusion errors due to DBT not reaching unbanked beneficiaries. Comparing the reach of Jan Dhan with that of Aadhaar suggests that the unbanked are more likely to constrain the spread of JAM than the unidentified.”

"Jan Dhan reality check: Manmohan Singh's criticism is indeed right but only partially")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

](https://images.firstpost.com/wp-content/uploads/2016/04/bankcounter-poor-380.jpg){kind=link}