"Reading in between lines: Where Raghuram Rajan goofed up")

Yesterday (20 September), the Reserve Bank of India (RBI) said it will:

- reduce the marginal standing facility (MSF) rate by 75 basis points from 10.25 percent to 9.5 per cent with immediate effect;

- reduce the minimum daily maintenance of the cash reserve ratio (CRR) from 99 percent of the requirement to 95 percent effective from the fortnight beginning 21 September 2013, while keeping the CRR unchanged at 4 percent; and

- increase the policy repo rate under the liquidity adjustment facility (LAF) by 25 basis points from 7.25 percent to 7.5 percent with immediate effect.

[caption id=“attachment_1085079” align=“aligncenter” width=“380”]

Raghuram Rajan should have clarified objectives, instruments and operating procedures in monetary policy. What he has done is confuse all issues.

PTI[/caption]

You did not understand that? Neither did I.

The challenge

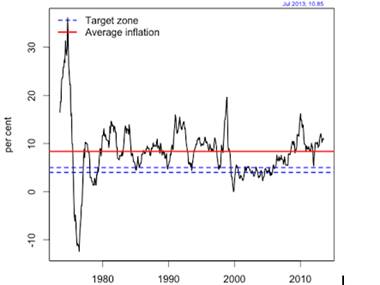

The heart of successful monetary policy is a coherent monetary policy_framework_. There should be clarity on objectives, instrumentsand operating procedure. The RBI has failed as a central bank because it lacks clarity on allthree. As a consequence, India has experienced sustained macroeconomicinstability: look at this long time-series of CPI inflation (see chart below):

[caption id=“attachment_1124825” align=“alignleft” width=“380”]  Chart[/caption]

Other than the 1999-2006 period, where we roughly achieved the goal of y-o-y CPI inflation from 4 to 5 percent, there has been failure all through.

One factor which is holding back high growth in India today is theimmense uncertainty about the future. What will happen to inflationand interest rates? Nobody knows, and this hurts confidence. There isa short-sighted view which suggests we should tolerate highinflation. But low inflation is a growth fundamental.

Matters have been made worse by the recent fight about the rupee (read here and here). Anarray of harmful measures were taken, which have muddied the watersconsiderably. The RBI operating procedure was shattered by thesemoves.

India now has the silliest monetary policy framework in the worldwhere the central bank engages in monetary policy through changes in eight numbers: (1) The repo rate, (2) The MSF/bank rate, (3) CRR (4), reverserepo rate, (5) LAF window cap, (6) MSF window cap, (7) minimum CRR to bemaintained, and (8) SLR. In addition, they also mess with capitalcontrols. A variety of objectives are in the fray including WPI, CPI,GDP growth, the exchange rate, exchange rate volatility, and thensome. So RBI is supposed to chase six objectives using nine instruments.

Raghuram Rajan did anexcellent Day 1 speech (on the day he was appointed as Governor). All of us were optimistic about what might arise in his work on monetarypolicy. What is required is clarifying objectives, instruments andthe operating procedure.

What we needed to say

Yesterday’s speech needed to say:

- RBI now has an unruly menagerie of objectives and instruments.

- This situation has generated heightened uncertainty which ishurting the economy.

- We got into this tangled mess because of the fear of QE (quantitative easing) withdrawal and the currency fight of recent months.

- We recognise that this is a mess.

- Now that this fear has subsided, we will clean things up.

- We do not care about the exchange rate. The prime objectiveof monetary policy is low and stable CPI inflation.

- We recognise that a central bank with discretion but not rulesis impotent. MIT and Yale teach Kydland and Prescott.

- We will replace this mess by a framework.

The announcements

In my reckoning, yesterday’s monetary policy statement has failed to clarify objectives, instruments and operating procedure.

As I read the statement, I could not understand whether this was a tightening or an easing. I spoke with veterans on the bond market and they were also fumbling. By the evening, it looked like the 91-day T-bill rate (one important summary statistic about the money market) had gone down by 20 bps, but the overnight interest rate swap (another important summary statistic about the money market) had gone up by 15 bps. Only late in the evening, I started thinking that it is an easing. The short end of the yield curve has gone down by 20-40 basis points (bps).

Some say that there is method in this madness, that an enormously complicated scheme is in motion which will make the world a nice place. But if a layman like me cannot understand the strategy that is now in motion, the fault lies in the statement.

Lack of clarity on objectives

The statement says that exchange rate volatility continues to be an objective at RBI: The timing and direction of further actions on exceptional measures will be contingent upon exchange market stability, and can be two-way. Further actions need not be announced only on policy dates.. I think this is a mistake. The only piece of sound macro policy in India today is the floating exchange rate. When RBI pursues exchange rate objectives (in whatever form), this leads to trouble.

And, this immediately begs the question: What is your objective? Are you targeting a specific exchange rate? Do you consider INR/USD volatility of over 15 percent annualised to be too high or too low? What statistical procedure will you use to measure volatility? The moment you try to answer these questions, you realise that the exchange rate is a bad objective. And, until the objectives are precisely stated, there is no monetary policy framework (RBI can hit the economy at random dates with random actions because they have committed themselves to nothing). There is also a loss of accountability which is the breeding ground for failure.

There is talk about both WPI and CPI. So the old confusion about the target continues. No serious economist thinks the WPI is a price index, so this talk reduces respect. There was talk about a WPI target of 6 percent. This suggests all is well, for WPI inflation is already there.

Messy outlook

Another disappointing thing that was made clear in the press conference was that capital controls will continue to be used. This is a mistake. In India, capital controls are not an effective tool for macroeconomic policy. Each attempt at doing this is going to roil the markets.

Far from saying that the messy defence of the rupee will be rapidly unwound, we are left worried that over the coming three years, in which QE will unwind, we will continue to have a messy framework.

Conclusion

Compare and contrast the press conference by Ben Bernanke - which is a masterpiece of clarity, against what we got from RBI.

The statement should have aimed to clarify objectives, instruments, and operating procedures. It has just intensified the muddle. And since the muddle - the lack of confidence in the macro framework - is India’s primary problem, it just made India’s problems worse.

Ajay Shah’s Blog "Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

](https://images.firstpost.com/wp-content/uploads/2013/09/Raghuram-Rajan-PTI-Feb27.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2013/09/ajaychart.png){kind=link}