"Think money is tight? RBI's QE was worth Rs 585,000 cr in the last six years")

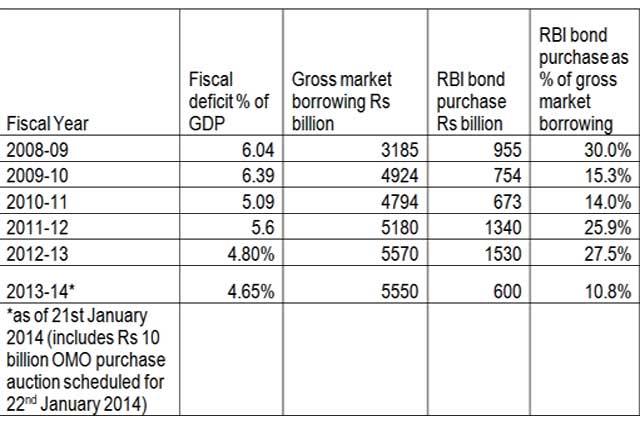

The RBI has been buying government bonds through OMO (Open Market Operations) bond purchase auctions since 2008-09. In the last six years, till the second half of January 2014, RBI has bought Rs 585,000 crore of government bonds.

[caption id=“attachment_1317597” align=“alignleft” width=“380”]  Representational Image. Reuters[/caption]

RBI has been funding the government by absorbing 10% to 30% of gross borrowing every year over the last six years. RBI does not see the bond purchases as back door deficit financing and looks at it as addition of liquidity into the system. The question is where does liquidity addition begin and where does deficit financing stop or vice versa?

Table above gives the yearly bond purchases of the RBI and percentage of gross government borrowing that it is funding.

What is OMO?

OMO or Open Market Operations is a tool of the RBI where it goes to the market to buy or sell bonds. RBI can buy or sell government bonds in the secondary market or it can buy or sell government bonds through sale/purchase auctions.

RBI, when it buys government bonds infuses primary liquidity into the system. The central bank is technically printing money to purchase government bonds. On the other hand when RBI sells government bonds, it takes money out of the system, which is a liquidity sucking measure.

RBI bond purchases through OMO is a form of QE (Quantative Easing). QE has gained popularity over the recent years as the Fed, Bank of England and Bank of Japan have been printing money to buy government bonds. Global central banks buy bonds to infuse cheap liquidity into the system to spur economic growth.

RBI has been fighting inflation over the last few years and has actually raised repo rates from as low as 4.75% to levels of 7.75%. Buying bonds to infuse liquidity even as interest rates were being raised is an anomaly as bond buying by printing money is seen as inflationary in nature.

The even more important question is, where has all the money gone? RBI has infused Rs 5850 billion into the system but the market is still borrowing money from the RBI to meet its daily requirements and has been doing so for the last three plus years. It is big question that neither the market nor the central bank seems to have an answer.

A central bank buying bonds when the government is borrowing and spending money gives rise to asset price bubbles. This could be one explanation for the multifold rise in property prices in India in the 2008-09 to 2013-14 period even as the economy floundered.

Arjun Parthasarathy is founder Investors are Idiots.com and INRBONDS.com. Follow him on twitter #arjunparthasara

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

](https://images.firstpost.com/wp-content/uploads/2014/01/RupeeNoteReuters.jpg){kind=link}