"Growth is not in RBI's hands; but a short rally is possible")

As attention focuses on the upcoming monetary policy announcement of the Reserve Bank of India (RBI), it’s safe to say that non-inflationary growth is out of the central bank’s hands. One could see an asset price inflation on monetary easing and the stock markets are already discounting it with the two-week rally.

Monetary easing often leads to growth, but any wealth accretion is quickly eroded by inflation. Sustainable growth is not triggered by monetary easing, it needs the creation of abundant goods and services. This is possible only when free markets are confident enough to invest and grow.

India’s policy muddle has frozen investments and output resulting in deceleration of production, which obviously puts an upward pressure on inflation. Decelerating output with rising money supply is the catalyst for inflation.

[caption id=“attachment_345912” align=“alignleft” width=“380” caption=“As attention focuses on the upcoming monetary policy announcement of the RBI, it’s safe to say that non-inflationary growth is out of the central bank’s hands. AFP”]  [/caption]

It’s in this context that a chorus of experts are calling for monetary easing and the RBI, in all probability, might oblige. Inflation in India is still running high and adding more money will only worsen the problem. It takes real reform of strong money and sustained industrial deregulation to spur long-term growth and arrest inflation. Think of the US in the 1980s, which adopted this approach. For two years the US economy went into a ditch as it cleared the monetary and regulatory excesses. It then roared back for a two-decade boom.

In India we have the Reserve Bank standing alone trying to fight inflation with tight money, on the one hand, but on the other hand, deficit financing by the government loosens money supply. Then we have the government refusing to deregulate and create growth that could not only lick inflation but cut deficits through increased tax receipts. So as one looks at the RBI for relief, don’t expect anything that will give investors the confidence to take a long term view of the economy.

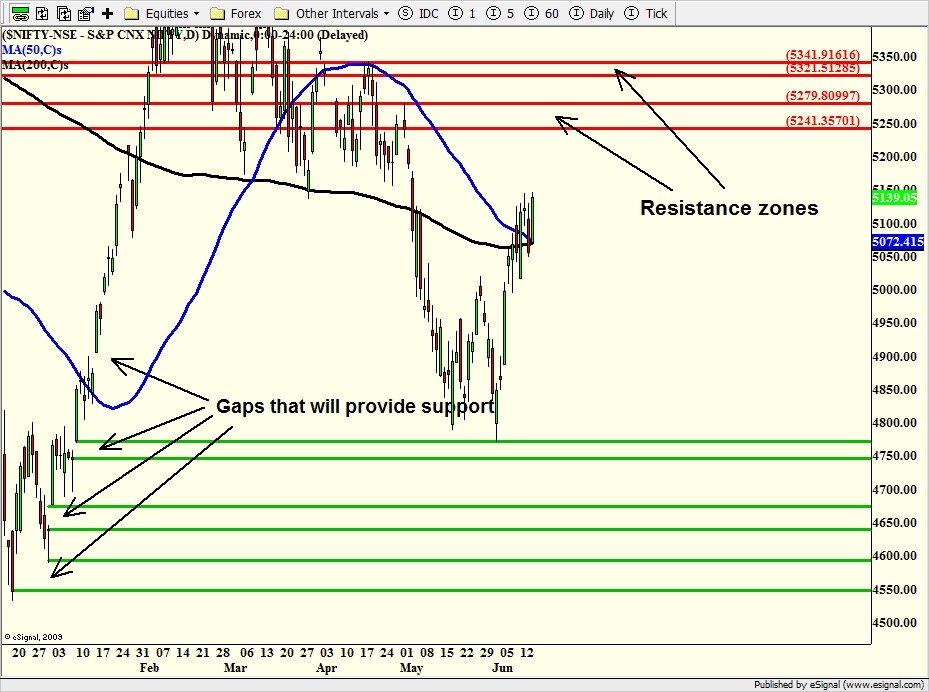

In case the RBI cuts rates or eases the cash reserve ratio (CRR), we could see a continuation of the rally that began on 4 June from the support level we had mentioned. A support level is where the demand for stocks exceed supply, which leads to a rally in price. A look at the charts of the Sensex ( Click here for Sensex chart ) and Nifty ( Click here for Nifty chart ) shows how much prices can rally.

Prices can go up to the resistance zones marked in red lines on the chart. Resistance zones are levels where the supply of stocks exceeds demand, due to which prices turn lower.

The indexes, however, have to close above Friday’s high to go higher. This is crucial as the market may have already discounted the RBI’s potential action and may not rally further. But if the RBI does nothing it will be bad for the markets.

Once prices reach the resistance zones, we expect a fall. Investors who bought stock should exit all or part of their positions a little below the resistance zones and book a profit. The resistance zones are also good areas to short the market. After the market reaches the resistance zones, we’d be in a better position forecast how much it can fall.

An analysis of the charts tells us that Nifty is relatively stronger than the Sensex and can hence reach resistance first and fall. It’s possible that the Sensex may never reach its resistance level and fall once the Nifty starts falling.

On a fundamental level, the bulls face a lot of headwinds. There are the Greek elections over the weekend and, if the leftist parties seeking to renege on austerity commitments win, we could see the markets fall. We also have rising yields in Spain and Italy, which could put a downward pressure on the markets.

As the cliche goes: these are dangerous times, play carefully.

George Albert is Editor, www.capturetrends.com

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

](https://images.firstpost.com/wp-content/uploads/2012/06/RBI-afp2.jpg){kind=link}

{kind=link}

{kind=link}