"As US rates rise, will equity crash or rally in short run?")

The equity markets seem oblivious to the fact that the 10-year treasury bond rate has risen around 45 percent since July 2012, when interest rates hit a new low of 1.4 percent. The 10-year rate stands today at 2 percent.

In spite of the slow rise in the treasury bond rate, the equity markets have been rising. After pumping trillions of dollars to bring interest rates down, the latest round of quantitative easing announced by the Federal Reserve aims to buy $85 billion worth of bonds each month for an unlimited time. Something does not seem right. When interest rates rise, the equity markets tend to fall. Also, when money supply is eased, interest rates fall. But that’s not happening.

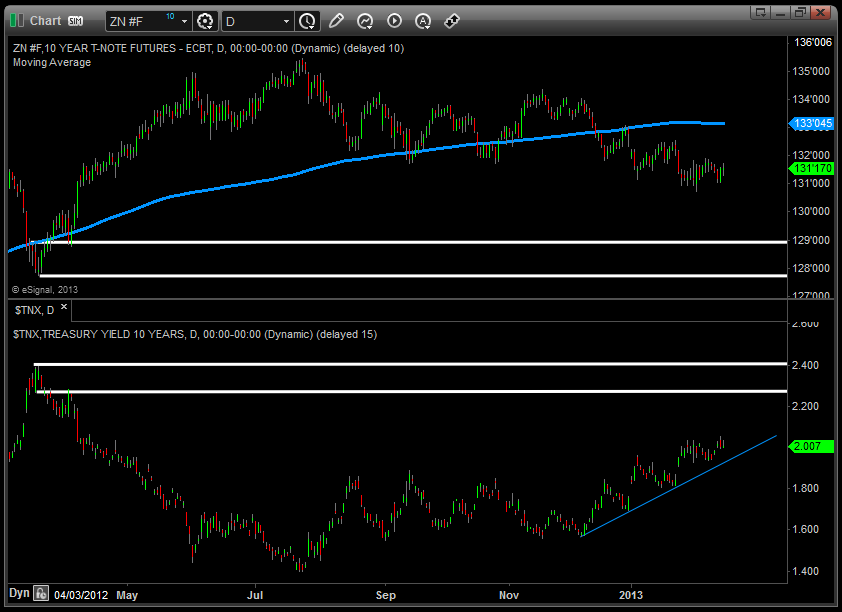

Let us first take a look at the chart of US treasuries ( click here for the chart ). The top charts shows the price of the 10-year US treasury bond and the lower chart shows the yield on those bonds. Notice that interest rates rise when bond prices fall. Despite all the money being pumped into the economy and, by extension, the globe, the Federal Reserve has failed to keep interest rates down and low. A lot of excess money printed by the Fed finds its way to the emerging markets as hot money, driving up those markets.

[caption id=“attachment_627748” align=“alignleft” width=“380”] 10-year T-rates could reach 2.25-2.5 percent levels from today’s 2 percent. That could result in a further slowing of the equity market uptrend or a reversal.[/caption]

Remember that the global stock markets are being held up by the availability of cheap money. What happens if the 10-year US treasury rate, which is a benchmark rate, continues to rise and money is no longer so cheap. Obviously the stock markets will correct. It has taken boatloads of freshly-printed money and super-low interest rates to pull a reluctant stock market to its 2007-08 peak. If that steroid loses effectiveness, as it seems to be with rising interest rates, the bulls will have nightmare on their hands.

It must be noted that the 10-year treasury price has been trading below its 200-day moving average for quite some time, which is bearish for bond prices and bullish for interest rates. The moving average is shown on the chart by the blue curving line. However, in the past the Federal Reserve has stepped in with huge amounts of cash and pushed up bond prices and the stock market. It could do it again, but the effectiveness may be drastically reduced.

Given the trend in the 10-year rate, it is possible that rates could rise to the levels marked by the two white horizontal lines and the bond prices fall to the level identified by the two horizontal lines. This essentially means that 10-year T-rates could reach 2.25-2.5 percent levels from today’s 2 percent. That could result in a further slowing of the equity market uptrend or a reversal.

The Bull’s View: The bullish view of this scenario is that the economy has entered a growth phase as a result of which the demand for money has gone up, leading to a rise in interest rates. With growth back on the table, the equity markets are continuing to rise despite rising interest rates. It is very possible that this scenario might be playing out right now.

Remember when the US was in a recession in 2000 and the Alan Greenspan Fed was cutting the Fed funds rate? It brought down interest rates from 6.5 percent in May 2000 to a low of 1 percent in 2003. All through this time the equity markets were falling. Then in June 2004 the Fed began increasing rates by 25 basis points at regular intervals till rates reached 5.25 percent in June 2006. During the rising interest rate regime and beyond till October 2007, the stock markets continued to rally. Most of the fizz in the markets was attributed to the excess money pumped into the system till June 2004 which put in place strong inflation expectations that led to the boom and bust of the real estate market.

So rising interest rates need not always lead to a fall in the equity markets unless the rates reach some inflection point. Then, the bust really hits hard and the recession that hit in 2007 took the S&P 500 below the recession lows of 2002. If the easy money policy of the early 2000s was the set-up for the spectacular bust of the late 2000s, what will the super-easy money beginning in 2006 lead to in the next few years? It is possible to have a stunning stock market rally followed by an equally stunning bust. Or the markets may wise up and take the route the Japanese markets took - that of slow decay.

The much higher debt burden of the US now compared to 2007 makes its economy highly susceptible to rising interest rates. So, for now, while the bull’s view may crystallise, we’d give more weight to the bearish view and keep an eye on rising interest rates given that the equity markets are already very high.

Nifty: The grip of the bear that we mentioned in last week’s article is still in place and got slightly tighter with the Nifty putting in new lows this week. The index has to close above the uptrending line and 50-day exponential moving average that we spoke about in last week’s article to loosen the bear’s grip. The support level mentioned in last week article is still in play.

George Albert is Editor, www.capturetrends.com

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

"Russian drones over Poland: Trump’s tepid reaction a wake-up call for Nato?")

"As Russia pushes east, Ukraine faces mounting pressure to defend its heartland")

"Why Mossad was not on board with Israel’s strike on Hamas in Qatar")

"Turkey: Erdogan's police arrest opposition mayor Hasan Mutlu, dozens officials in corruption probe")

{kind=link}