"An apocalyptic end to the dollar hegemony is coming")

By Dee Woo

The US debt crisis and the recent downgrade of its sovereign rating by rating agency Standard & Poor’s have brought the whole world to a point where there’s great uncertainty about the future. Nobody knows how to respond to a possible US default.The whole world has taken the US’s solvency for granted for way too long. The global trade boom has been so heavily collateralised against the US deficit that we don’t know how it will function in an alternative scenario.

World trade today is a game in which the US produces dollars and the rest of the world produces things that dollars can buy. All the other central banks need to accumulate dollars to keep their currency undervalued against the dollar and retain comparative trade advantage. So what happens if the US government goes bankrupt and the dollars become worthless?

This is really a wake-up call. The world needs to decouple its well-being from the US deficit. We can’t delay the inevitable forever, because next time it will be more than just a close call.

We need to be prepared for a world without the dollar as the dominant reserve currency, and without the US consumption economy as the vital export growth engine. We need the Euro to step up and take over more responsibilities from the dollar. And we need China to unleash a consumption economy to help address the global imbalance.

[caption id=“attachment_73812” align=“alignleft” width=“380” caption=“The world needs to decouple its well-being from the US deficit.Getty Images”]  [/caption]

Otherwise, the world economy will continue to run on inertia - until the dollar and the US consumption economy can no longer support the weight placed on them.

The world has prospered on the debt-fuelled credit binge in the US for decades. Yet, all good things must come to an end.

The dollar hegemony is a curse even to the US

The dollar hegemony has become the US’s biggest disincentive to maintain its fiscal and monetary discipline. According to a report by the Division of Monetary Affairs from the Federal Reserve, since 1990 the US monetary expansion has been driven by the dominant external demand for the dollar. Hundred-dollar notes are the largest denomination now issued by the Federal Reserve, which make up 60 percent of the dollar value of all the US currency outstanding.

The data on the use of $100 notes suggests that the net new demand for them is coming predominantly from abroad. On average over the 1990s, the overseas stock of dollars has been growing about three times faster than the domestic stock. Empirically, the amount of currency outstanding typically grows in sync with, or even a little more slowly than, consumption in the United States.

Indeed, this was the pattern until 1990. However, in the decade after 1990, in tune with the growing external demand for dollars, the US currency grew about 3.5 percentage points faster than consumption in nominal terms. Some may be inclined to suggest these overseas dollars will probably be used to buy US goods and service and therefore boost US employment.

So, where’s the money?

Nothing can be farther from the truth. The majority of the overseas dollars are parked in US Treasuries and other dollar-denominated securities and assets by courtesy of the official foreign exchange holdings and Eurodollar market. They are fuelling a debt-financed domestic demand in the US, which explains the self-enforcing mechanism of the US twin deficits (trade deficit and fiscal deficit).

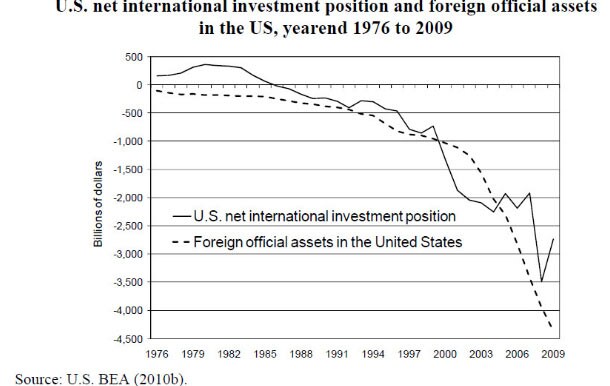

According to Professor Robert A. Blecker’s research, by the end of 2009, foreign central banks had assets of $4.4 trillion in the US , some 60 percent higher than the overall US net debtor position of $2.7 trillion ( see chart ). That is to say, excluding this colossal debt to foreign central banks, the US was still a net creditor country to the tune of about $1.7 trillion in all of its other unofficial that is, non-central bank) international financial activities as of end-2009.

Hence, the expanding foreign accumulation of US assets after 2000 was not primarily driven by the increased confidence in the US economy or US assets by private-sector agents abroad, as contemplated in the models of “ capital market imperfections.” On the contrary, it was mainly foreign central bank intervention that financed the growing US twin deficits. The dollar’s dominance has done the US a huge disservice as it struggles to maintain its fiscal and monetary discipline: it has facilitated a vicious circle of twin deficits and weak dollar policy by the Federal Reserve. The nature of self-destruction that lies down this path is very clear.

Second, the fact that the US’s money multiplier and velocity are greatly dictated by foreign agents because of the dollar hegemony has rendered the federal reserve increasingly ineffective as a domestic central bank, especially in the time of recovery.

Continues on the next page

European banks are laughing all the way…

As financial blog Zerohedge’s research shows (citing the Fed’s Bloomberg FOIA release), the majority of the dollars generated by QE2 were funnelled to foreign banks (especially European banks) instead of US banks_._ Among the 20 Primary Dealers currently recognised by the New York Fed, 12 are foreign. The Eurodollar market- which accounted for nearly 90 percent of all international loans by 1997 - enables a skewing of reserve balances towards foreign banks operating in the US.

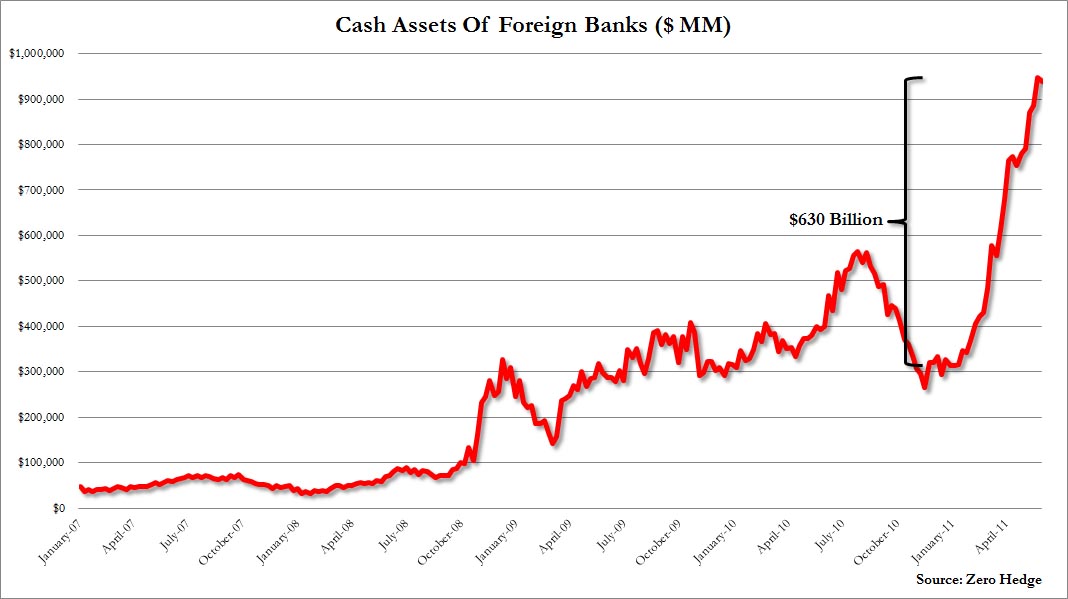

Foreign banks operating in the US often lend reserves to home offices or other banks operating outside the US, and do not account for a large percentage of consumer or real estate loans. Foreign banks represent about 16 percent of commercial bank assets and only about 9 percent of bank credit: in other words, they add far less value to the average American than domestic banks - and yet they obtain a disproportionate amount of assistance – directly or indirectly - from the US government . Thus, the notion that excess reserves enhance lending activities and money growth is greatly diminished by the skewing of excess reserve balances toward foreign banks. The truth is that cash assets held by foreign banks operating in the US grew more than six times between the fourth quarter of 2008 and the third quarter of 2010, and have more than tripled again this year.

[caption id=“attachment_73816” align=“alignleft” width=“380” caption=“The dollar hegemony will come to an end by either a forceful market correction or a gradual reconstruction of the global reserve currency system.Getty Images”]  [/caption]

So, why has US bank lending remains stagnant even though the Fed has pumped so much money into the system? Research by Stone McCarthy’s has noted that affiliated foreign branches of US banks tend to borrow dollars in the Eurodollar market. Given that a Eurodollar is nothing more than a dollar-denominated deposit at a bank outside the US, the bank holding the Eurodollar deposit will ultimately have a dollar-denominated claim against a bank domiciled in the US. That US bank in turn holds reserve balances at their local Federal Reserve banks, so when Eurodollar deposits move from one foreign bank to another, the claim against the original US bank follows the Eurodollar deposit.

**Who gained from the QEs?**Not the US…

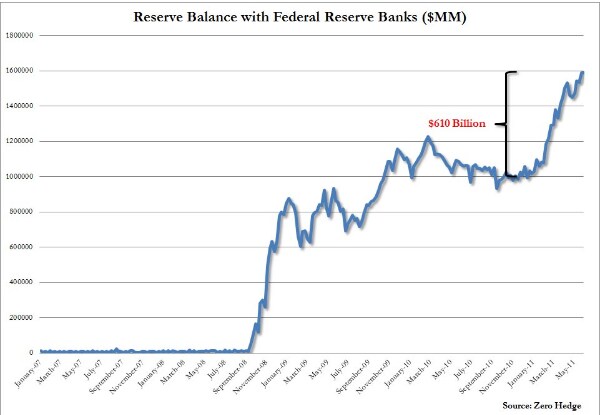

If a bank domiciled in the US borrows dollars from a bank outside the US, effectively what happens is that the reserve balance of the US bank underpinning the Eurodollar account is reduced, and the reserve account of the borrowing bank in the US is increased. Overall, US bank reserves are left unchanged, but the distribution of those reserves is changed from one bank in the US to another, possibly even from the books of one Federal Reserve Bank to another. There was a $630 billion increase in foreign bank cash balances in the US between November 2010 and May 2011 ( see chart) , which coincides neatly with the date when the Fed commenced QE2. During the same period, Fed reserves saw a $610 billion increase. ( see chart)

By comparison, how did cash held by US banks fare as a result of QE2? Not well. Cash balances at small and large US domestic banks did not increase to the same extent as cash at foreign banks ( see chart ); as was the case with QE1, most of the dollars created by QE2 went to foreign banks.

This is the curse of the dollar as the world reserve currency. With the powerful Eurodollar market and near-zero domestic interest rates, the Federal Reserve has become a rather impotent domestic central bank as the recovering US economy continues to struggle in a liquidity trap and the dollar chases yield.

But there is no alternative to the dollar

The dollar hegemony has become fiscally and monetarily unsustainable to the US itself. The dollar hegemony will come to an end by either a forceful market correction or a gradual reconstruction of the global reserve currency system. The best candidate in this reconstruction used to be the Euro.

However, it is difficult to imagine that the currency of a continent so battered will be strong enough to replace the dollar at the world’s reserve currency anytime in the near- or medium-term. Among the leaders of the Euro bailout, France is battling a possible rating downgrade, and Germany is threatened with an upcoming constitutional crisis due to the hysterical national backlash against the bailout. The expansion of euro rescue funds has simply become economically, politically and fiscally unsustainable for the two leading countries. Under these circumstances, it is hard to imagine how the Euro will survive the current crisis.

The Chinese yuan (or the renminbi) will not join in the race to be a world reserve currency in the foreseeable future. At best it can act as a regional invoicing currency among trading partners. That’s because China has some insurmountable flaws when it comes to pitching the yuan as a candidate as a world reserve currency: it has a political structure that shares no aspirations with democratic economies, powerful state control over economic issues, an overmanipulated exchange rate, an impotent law system that does not protect property rights, and fragile diplomatic relationships with many trading partners.

In the absence of a meaningful alternative, the global currency system will in all likelihoods continue to hobble along using the wounded dollar until the final day of reckoning. If the dollar and the US treasury market do collapse next time, the firesale of T-bills will paralyse the repo market, drive up borrowing costs, suck dry the liquidity and close up the spread in the carry trade. The ensuing panic will be contagious. Many financial institutions will fall, including some gigantic sovereign funds. The global financial system as we know will be utterly destroyed.

Dee Woo is an economics lecturer at the Beijing Royal School and a columnist in leading journals.

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

](https://images.firstpost.com/wp-content/uploads/2011/08/dollar-burning.jpg){kind=link}

{kind=link}

](https://images.firstpost.com/wp-content/uploads/2011/08/dollar3.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}