The overall expenditure of Jet Airways was simply too high, given the total income of the airline. A basic problem with the business model

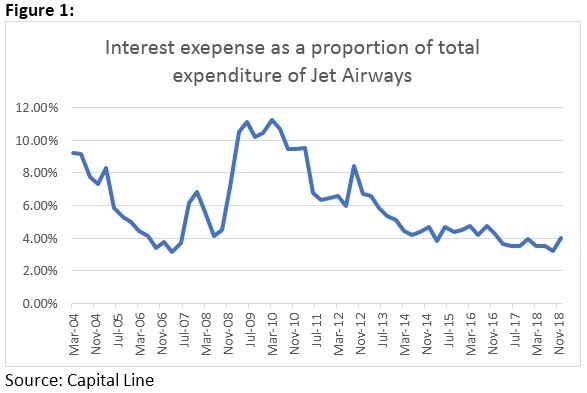

Editor’s note: This is part of a multi-article series on the downfall of Jet Airways and the path ahead for the cash-strapped airline. It’s been close to three weeks since Jet Airways temporarily shut its operations. The jury is still out on how and why, what was India’s largest private airline, once upon a time, reached a stage where it had to shut down the operations. The general perception seems to be that the airline borrowed more than it was in a position to repay. Eventually, it didn’t have enough money to pay interest on its debt and that led to the temporary grounding. But that, as we shall see, was not the major reason for India’s oldest private airline shutting its operations. [caption id=“attachment_94955” align=“alignleft” width=“380”]![Representational image. Reuters.]() Representational image. Reuters.[/caption] Let’s take a look at the issue point wise. 1) For the period October to December 2018, the last available financial results of the airline, the total income of the airline stood at Rs 6,198.38 crore. Against this, the expenditure of the airline stood at Rs 6,418.87 crore. The interest cost on the debt of the airline, during this period had stood at Rs 220.49 crore. As a proportion of total expenditure of the airline, the total interest cost was 4 percent. Yes, just 4 percent. Nearly 96 percent of the expenditure happened on other things. 2) And this was not a one-time thing. Take a look at Figure 1, which basically plots interest expense as a percentage of expenditure for the airline over a period of 15 years.

Representational image. Reuters.[/caption] Let’s take a look at the issue point wise. 1) For the period October to December 2018, the last available financial results of the airline, the total income of the airline stood at Rs 6,198.38 crore. Against this, the expenditure of the airline stood at Rs 6,418.87 crore. The interest cost on the debt of the airline, during this period had stood at Rs 220.49 crore. As a proportion of total expenditure of the airline, the total interest cost was 4 percent. Yes, just 4 percent. Nearly 96 percent of the expenditure happened on other things. 2) And this was not a one-time thing. Take a look at Figure 1, which basically plots interest expense as a percentage of expenditure for the airline over a period of 15 years.

![JET FIGURE 1]()

Figure 1 makes for a very interesting reading. In the last five years, the interest on debt as a percentage of total expenditure was around 4.1 percent. There was an era when interest as a proportion of the total expenditure of Jet Airways was more than 11 percent. This isn’t surprising given that the total debt of the airline had reached a high of Rs 16,323.53 crore in March 2009. By March 2018, it was down to Rs 8,403.15 crore. 3) What does this tell us? It basically tells us that the interest expense and the total debt of the airline was basically the straw that broke the camel’s back. The basic problem lay somewhere else. The overall expenditure of Jet Airways was simply too high, given the total income of the airline. A basic problem with the business model. It just wasn’t making enough money to be a viable business, to justify all the money already invested in the airline. It also tells us that when it comes to airlines, India is a very price-sensitive market and people keep flying, only if tickets are available at a reasonable price. The moment they go beyond a certain price, people move to other forms of travel. In that sense, airlines do not have much pricing power to drive up their revenues beyond a point. The way to increase revenue is to fly newer routes. But that needs newer aircraft (even if they are leased) and it means higher expenditure. 4) Indeed, much of it sounds like what Warren Buffett used to say about airlines, when he did not invest in them. As he said in one of the letters to the shareholders of Berkshire Hathaway: “The worst sort of business is one that grows rapidly, requires significant capital to engender the growth, and then earns little or no money. Think airlines. Here a durable competitive advantage has proven elusive ever since the days of the Wright Brothers. Indeed, if a farsighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favor by shooting Orville down.” Things have changed since Buffett said this and he now invests in airlines. Jet Airways was specifically the kind of business that Buffett warned investors against. It did not scale well. Let’s take a look at the numbers over a long period of time. In the period of three months ending March 2004, the total income of the airline was Rs 961.13 crore, with the expenditure being Rs 682.1 crore. In the period three months ending December 2018, the total income of the airline stood at Rs 6,198.38 crore, a jump of 545 percent. The expenditure had increased to Rs 6,418.87 crore, a jump of 841 percent. The expenditure of the airline over a period of 15 years has been growing much faster than its income, which basically tells us that the airline does not have a durable business model (lack of competitive advantage that Buffett talks about). Or to put it simply, the airline did not benefit from economies of scale as the income went up, expenditure went up as well, at a faster rate. 5) What also has not helped is the fact that the airline simultaneously tried to operate both in the low-cost space as well as full-service space. Other than creating a brand confusion in the mind of the user, it also creates other operational difficulties. This is a problem which no-frills carriers like SpiceJet, GoAir and IndiGo, which have concentrated on one area, the low-cost space, haven’t had to face. 6) As far as the future of the debt-laden airline is concerned, there doesn’t seem much hope for the simple reason that it is easier to sell a functional airline than a non-functional one. The real value of any airline comes from the code sharing agreements it has in place and the slots that it has at airports. In airports across India, some of these slots have been temporarily allocated to other airlines. Many pilots have already left Jet Airways to work for other airlines. 7) In this scenario, it seems very difficult for the airline to fly again. What is also not helping is the fact that the Lok Sabha elections are underway, and any significant decision from the government’s end, given that the airline owes a lot of money to the public sector banks, is unlikely to happen before the next government is formed and starts functioning. That means nearly three weeks more. Every day of non-operation basically increases the probability of the airline not flying again. (The writer is an economist and the author of the Easy Money trilogy) Part 1:

Govt can mount Satyam-type rescue on cash-strapped airline and make money on it as a smart investor Part 2:

How Naresh Goyal’s airline walked into a trap of its own making from where there was no return Part 3:

Downfall of Jet Airways: Banks had seen writing on the wall with over a billion dollars to be paid back, but yet acted too late

"Downfall of Jet Airways: Debt-laden airline never had a viable business model, failed to maintain income-expenditure balance")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")