"The S&P is wrong about Manmohan and Sonia")

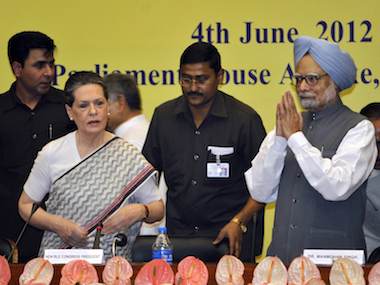

Standard & Poor’s has warned India its sovereign debt rating could fall from investment grade. A debt rating is a score given to countries and companies, marking them on how secure the debt that they issue is. S&P has been aggressively downgrading countries in the recent past, and there was surprise when they cut the rating of the United States a few months ago from AAA to AA+. India’s rating is BBB-, which is the lowest possible investment grade. India got the rating five years ago, the poorest nation in the world ever to get an investment grade rating. In comparison, China’s is AA-, while Pakistan’s is B-, which places it in the junk bonds category. The rating is based on economic and financial data. However, an element of analysis is included. To see how subjective this analysis can be, consider what S&P’s Joydeep Mukherji said while explaining why the firm had cut the United States’s rating. This had been done, he said, because of Republican skepticism last year (during budget negotiations) that a US debt default would be particularly damaging. “This kind of rhetoric is not common among AAA sovereigns,” said Mukherji. [caption id=“attachment_346542” align=“alignleft” width=“380” caption=“Indian Prime Minister Manmohan Singh, right, and Congress Party President Sonia Gandhi, arrive at a meeting of the Congress Working Committee in New Delhi, India, Monday, June 4, 2012. AP”]  [/caption] Mukherji is incidentally one of the two authors of the India report. The other author is Takahira Ogawa, who pained India by cutting its outlook to ‘Negative’ from ‘Stable’ after a visit to Delhi a couple of months ago. This cut was a warning that a downgrade was possible within 36 months if economic indicators did not pick up. S&P fears India might be the first of the BRIC (Brazil, Russia, India and China) nations to join Pakistan in the speculative grade or junk bond category. Mukherji and Ogawa say S&P will not downgrade India if the following happens: “modest steps” in cutting growth in spending, 7 percent or more GDP growth, “modest progress” in reducing the fiscal deficit and “some” reforms and administrative measures. They warn that S&P will downgrade India if the following happens: Growth in spending and “lower-than-projected” GDP growth, increasing the fiscal deficit. So far so good and this sounds reasonable. A higher fiscal deficit crowds out the private sector (because the government is also borrowing heavily) making access to capital expensive and that’s bad for business. The two men then offer a political analysis for the reasons why things are bad, and here the report begins to slip. The analysis is under the headline: “Divided leadership at the center may be the biggest hurdle”. S&P explains how Sonia Gandhi is the real political force, and Manmohan Singh is an appointed prime minister. This division “has weakened the framework for making policy” and “has likely contributed to poor discipline and cohesion.” The problem is that there is no alternative. Real power will always remain with Sonia Gandhi because Congress is a dynastic party. But she’s not qualified to become prime minister. She’s never been to college and her main educational qualification according to her Lok Sabha resume is passing out of high school. Mukherji and Ogawa ought to have given an example of something that divides Manmohan and Sonia along policy, but they cannot because Manmohan and Sonia have an excellent relationship. One that, in my opinion, works. She trusts him to think up high policy and execute it while she tries, sometimes failing, to give him the power to push this through. Sonia as prime minister making policy decisions on her own, or her stepping aside to let a Congressman take full charge are both unworkable. Division of opinion on reforms both inside the Cabinet and even inside the Congress will remain in a nation as diverse as India. That is why it is easy to make petrol expensive but not so easy to cut subsidy on diesel or LPG or increase railway passenger fares. The critical issue is whether Manmohan believes that social spending is economically beneficial. He very strongly believes it is. I think he would have stepped down if he did not agree with the enormous spending on NREGA or Right to Education. He has said in interview that the major reforms have already been legislated. I think he’s right. The key to sustained growth cannot be the passing of vestigial reforms like more foreign investment in retail. An economy whose base is a very low $1500 per capita must have an internal dynamic to grow in sustained fashion. A healthy population that has access to quality education is critical. Neither is available to India today, with more malnourished, illiterate and half-literate people than any other nation. Manmohan is right to try and thread the needle between high social spending and a fiscal deficit on the cusp of manageability. His hope, and it can be no more than that, is that this spending produces the nourishment to make the seeds sprout. The S&P report’s analysis, prescriptions and its threats must be put in perspective in this light.

Authors Mukherji and Ogawa say S&P will not downgrade India if the following happens: “modest steps” in cutting growth in spending, 7 percent or more GDP growth, “modest progress” in reducing the fiscal deficit and “some” reforms and administrative measures.

Advertisement

End of Article

Written by Aakar Patel

Aakar Patel is a writer and columnist. He is a former newspaper editor, having worked with the Bhaskar Group and Mid Day Multimedia Ltd. see more

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

](https://images.firstpost.com/wp-content/uploads/2012/06/sonia1.jpg){kind=link}