The hope now is that the RBI will cut the repo rate further, banks will cut the interest rates on their loans and deposits, and people will borrow and spend

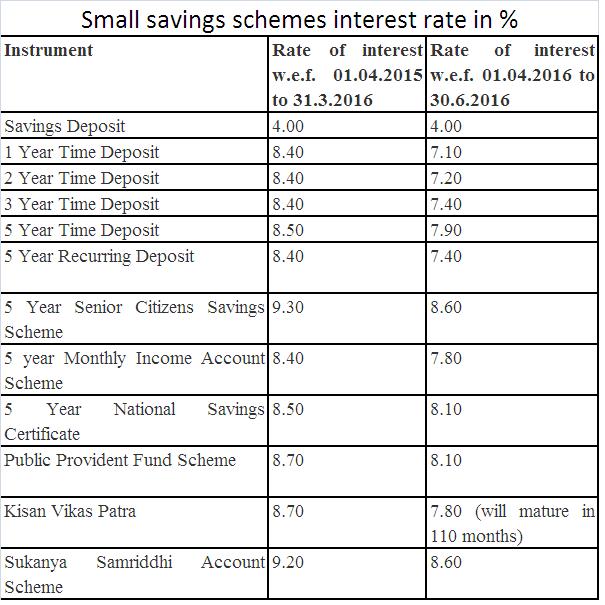

The Narendra Modi government has cut the interest rates on offer on the public provident fund(PPF) and other small savings schemes run by the post office. The new interest rates will come into play from April 1, 2016 and will be in effect until June 30, 2016. The interest rate on PPF has been cut from 8.7% to 8.1%. The interest on the Senior Citizens Savings Scheme has been cut from 9.3% to 8.6%. This decision to cut down interest rates hasn’t gone down well with the middle class. This has come soon after the Employees’ Provident Fund(EPF) fiasco where the government tried to tax the accumulated corpus of the private sector employees on contributions made after April 1, 2016. [caption id=“attachment_2685490” align=“alignleft” width=“380”]

Reuters[/caption] While trying to tax EPF was incorrect, the hue and cry being made out on interest rates on PPF and small savings schemes being cut, is uncalled for. This is happening primarily because most people have become victims of what economists call the money illusion. What is money illusion? As Gary Belsky and Thomas Gilovich write in Why Smart People Make Big Money Mistakes: “[Money illusion] involves a confusion between ‘”nominal” changes in money and “real” changes that reflect inflation…Accounting for inflation requires the application of a little arithmetic, which…is often an annoyance and downright impossible for many people…Most people we know routinely fail to consider the effects of inflation in their finance decision making.”

![Small-savings-interest-table]()

Hence, money illusion is essentially a situation where people don’t take inflation into account while calculating their return on an investment. How does this apply to the current context? Let’s consider the Senior Citizens Savings Scheme. The interest rate on offer on the scheme was 9.3%. The rate of inflation that prevailed between 2008 and 2013 was 10% or more. Hence, the real rate of return on the scheme was negative. This was the case with other small savings schemes as well as bank fixed deposits. In fact, the real rate of return was well into the negative territory. The real rate of return for a senior citizen who did not have to pay income tax on the earnings from the Senior Citizens Savings Scheme stood at minus 0.7% (9.3% minus 10%). For those who had to pay income tax, the real rate of return was even lower. For those in the 10% tax bracket the real rate of return was minus 1.63% per year. For those in the tax 20% and 30% tax brackets, the real rate of return was minus 2.56% and minus 3.49%. But back then no one complained about the interest rate being low, even though almost everyone who invested in PPF and other small savings, was losing money. The purchasing power of their investment was coming down. The situation is totally different now. Inflation as measured by the consumer price index stood at 5.2% in February 2016. Given this, the real rate of return is now in positive territory. Let’s repeat the Senior Citizens Savings Scheme example and see how the real returns stack up. The interest rate on offer on the Senior Citizens Savings Scheme from April 1, 2016, is 8.6%. For those who do not have to pay any income tax, the real rate of return is 3.4% (8.6% minus 5.2%). For those in the 10%, 20% and 30% tax brackets, the real rate of return works out to 2.54%, 1.68% and 0.82% respectively. Hence, the situation is substantially better than it was in the past. Investors are actually making a real rate of return on their investments. Also, for savings instrument like PPF, where no tax needs to be paid on accumulated interest, the real returns are higher. But given that the nominal interest rate has been cut, people have an issue and a lot of noise is being made. Given these reasons, the government was right in cutting the interest rates on offer on PPF and other small savings schemes. Also, it is important to understand that the high rates of interest on offer on these schemes has been preventing the banks from cutting their deposit as well as lending rates at the speed at which the Reserve Bank of India wants them to. As RBI governor Raghuram Rajan had said in December 2015 “Since the rate reduction cycle that commenced in January [2015], less than half of the cumulative policy repo rate reduction of 125 basis points [one basis point is one hundredth of a percentage] has been transmitted by banks. The median base lending rate has declined only by 60 basis points.” Repo rate is the rate at which RBI lends to banks. While RBI cut the repo rate by 125 basis points in 2015, the banks only managed to pass on less than half of that cut to their end consumers. One reason for this is that many public sector banks have had a huge problem with their corporate loans. Another reason has been the high interest rates on offer on small savings schemes. The banks compete with these schemes for deposits and given the high interest on offer on post office savings schemes, banks could not cut interest rates beyond a point without losing out on deposits. The hope now is that the RBI will cut the repo rate further, banks will cut the interest rates on their loans and deposits, and people will borrow and spend. Whether that happens remains to be seen. (Vivek Kaul is the author of the Easy Money trilogy. He tweets @kaul_vivek)

"Govt cutting PPF, small savings rates is good; now it is RBI's turn")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

"Charlie Kirk, shot dead in Utah, once said gun deaths are 'worth it' to save Second Amendment")

"From governance to tourism, how Gen-Z protests have damaged Nepal")

"Did Russia deliberately send drones into Poland’s airspace?")

"Netanyahu ‘killed any hope’ for Israeli hostages: Qatar PM after Doha strike")

](https://images.firstpost.com/wp-content/uploads/2016/03/india-post-380-rtrs.jpg){kind=link}