"Banks in trouble after cancellation of 2G licences")

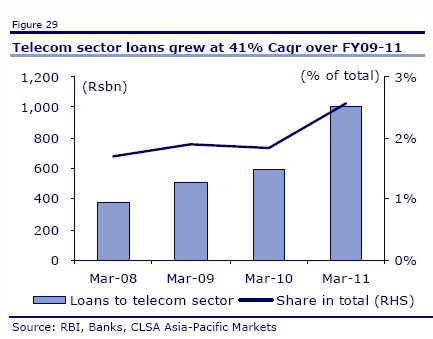

Telecom sector loans form 3 percent of the total banking portfolio. It makes up for 19 percent of infrastructure loans as well. The telecom sector has been under the radar for quite sometime. But with 122 licences cancelled, the banks which have leant extensively could be in deep trouble.

A closer look at individual exposure Yes Bank has the maximum exposure in terms of percentage of loan book. Its exposure stands at 5 percent. Canara Bank, PNB, Axis Bank, Bank of Baroda, Oriental bank of Commerce, SBI, Corporation Bank and HDFC Bank have more than 1 percent of their loan book exposed to the sector.

The lenders give money against the guarantee of the licence. When licences are cancelled the underlying asset is no more and the loan will in all probability will turn into a bad asset.

The percentage of loan book exposure to the sector however does not necessarily signal a corresponding percentage threat to the bank. For example, Yes Bank could have its exposure to an incumbent telecom company and therefore might face no threat to its portfolio. Yes Bank’s spokespersons have also clarified that the company does not have any exposure to the 2G license that have been cancelled. In that case, bank exposures have to be examined at an individual basis to understand the real threat.

Moreover, banks which have exposure to the equipment suppliers in the telecom space will also suffer as their loan repayment will be in jeopardy now.

Punjab National Bank, CNBC Tv 18 reports has exposure to all the companies whose licences have been cancelled. The stock is down 3 percent.

Impact Shorts

More ShortsSBI which also has significant exposure to the sector has said they have lent to strong companies and will now work out how costs can be recouped with individual companies.

For now, some other bank stocks have reacted negatively to the judgement. Yes Bank is down 1 percent, SBI is down 3 percent, Axis Bank is down 1.7 percent.

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

"Israel targets top Hamas leaders in Doha; Qatar, Iran condemn strike as violation of sovereignty")

"Nepal: Oli to continue until new PM is sworn in, nation on edge as all branches of govt torched")

"Who is CP Radhakrishnan, India's next vice-president?")

"Israel informed US ahead of strikes on Hamas leaders in Doha, says White House")

](https://images.firstpost.com/wp-content/uploads/2012/02/telecom.jpg){kind=link}

](https://images.firstpost.com/wp-content/uploads/2012/02/telecom1.jpg){kind=link}