It is a tale of two acquisitions by the same group. While one failed miserably, the other succeeded surprisingly. The stories are about Tata Steel’s acquisition of Anglo Dutch major Corus and Tata Motors’ buyout of Jaguar Land Rover (JLR) of the UK. Here’s how the stories unfolded. Tata Steel completed acquisition of Corus on 2 April 2007, at the peak of the boom that ended with the Global Financial Crisis in 2008, from which the world economy never recovered. The company early on Wednesday said it is exploring “all options for portfolio restructuring, including the potential divestment of Tata Steel UK, in whole or in parts”. Corus was renamed Tata Steel Europe in 2010. [caption id=“attachment_2706664” align=“alignleft” width=“380”]

Reuters[/caption] The decision to sell the UK business comes at a time when the global economy is staring at a further recession, this time driven by a Chinese meltdown. Explaining the rational behind the decision, Tata Steel said in a statement: While the global steel demand, especially in developed markets like Europe, has remained muted following the financial crisis of 2008, trading conditions in the UK and Europe have rapidly deteriorated more recently, due to structural factors including global oversupply of steel, significant increase in third country exports into Europe, high manufacturing costs, continued weakness in domestic market demand in steel and a volatile currency. In simple terms, what the company is saying is that cheap Chinese steel dumped across the globe has rendered the business unviable in the face of the continuing financial crisis impact. For the beginners, Corus acquisition paved the way for the Tatas to enter the UK steel sector. The acquisition was preceded by an unprecedented takeover battle with Brazilian major CSN. Here’s how the battle played out: The Tata group confirmed its interest in Corus on 5 October 2006 and proposed a bid of 455 pence a share in cash on 17 October. On 17 November, CSN offered 475 pence. In response, Tatas upped the bid to 500 pence a share. Then CSN raised the bid to 515 pence a share. As the bidding war heated up, UK Takeover Panel decided to auction the company on 30/31 January. In a nail-biting finish for the seven-hour long bidding war, the Tata group won offering 608 pence a share, 34 percent higher than its original bid. The total payment was $12.1 billion (Rs 53,580 crore at the then exchange rate), of which $6 billion was debt. Justifying the price the company paid, then group chairman Ratan Tata said in an

interview

to the Business Standard: Investors came in and increased the price. We have to pay for getting the company. As a prudent management, we had taken a view that we would not go beyond a point. We did not reach that point. Had we reached, we would have walked away. Overbidding or not is subjective when it comes to a judgement call. Stock investors were not happy with Tata Steel’s aggressive bidding. Right from the day the Tatas expressed their keenness to buy Corus on 5 October 2006, investors had pummelled the stock. Over the next six months the stock fell 21 percent. A day after the Indian company won the bid, the stock fell 11 percent. Over a month, it fell 20 percent. Ratan Tata, however, defended his group’s decision, saying the market is taking a short-term view and is being harsh. “We often damn a company when it makes a loss in a single year. We applaud a company when it makes an extraordinary profit. But the life of a corporation is much longer than a single year,” he told Business Standard. However, at least in the case of Tata Steel, the markets seem to have been bang on target with the bearish view. Here are eight graphics that shows how the acquisition dented the fortune of the Tata Steel group:

Reuters[/caption] The decision to sell the UK business comes at a time when the global economy is staring at a further recession, this time driven by a Chinese meltdown. Explaining the rational behind the decision, Tata Steel said in a statement: While the global steel demand, especially in developed markets like Europe, has remained muted following the financial crisis of 2008, trading conditions in the UK and Europe have rapidly deteriorated more recently, due to structural factors including global oversupply of steel, significant increase in third country exports into Europe, high manufacturing costs, continued weakness in domestic market demand in steel and a volatile currency. In simple terms, what the company is saying is that cheap Chinese steel dumped across the globe has rendered the business unviable in the face of the continuing financial crisis impact. For the beginners, Corus acquisition paved the way for the Tatas to enter the UK steel sector. The acquisition was preceded by an unprecedented takeover battle with Brazilian major CSN. Here’s how the battle played out: The Tata group confirmed its interest in Corus on 5 October 2006 and proposed a bid of 455 pence a share in cash on 17 October. On 17 November, CSN offered 475 pence. In response, Tatas upped the bid to 500 pence a share. Then CSN raised the bid to 515 pence a share. As the bidding war heated up, UK Takeover Panel decided to auction the company on 30/31 January. In a nail-biting finish for the seven-hour long bidding war, the Tata group won offering 608 pence a share, 34 percent higher than its original bid. The total payment was $12.1 billion (Rs 53,580 crore at the then exchange rate), of which $6 billion was debt. Justifying the price the company paid, then group chairman Ratan Tata said in an

interview

to the Business Standard: Investors came in and increased the price. We have to pay for getting the company. As a prudent management, we had taken a view that we would not go beyond a point. We did not reach that point. Had we reached, we would have walked away. Overbidding or not is subjective when it comes to a judgement call. Stock investors were not happy with Tata Steel’s aggressive bidding. Right from the day the Tatas expressed their keenness to buy Corus on 5 October 2006, investors had pummelled the stock. Over the next six months the stock fell 21 percent. A day after the Indian company won the bid, the stock fell 11 percent. Over a month, it fell 20 percent. Ratan Tata, however, defended his group’s decision, saying the market is taking a short-term view and is being harsh. “We often damn a company when it makes a loss in a single year. We applaud a company when it makes an extraordinary profit. But the life of a corporation is much longer than a single year,” he told Business Standard. However, at least in the case of Tata Steel, the markets seem to have been bang on target with the bearish view. Here are eight graphics that shows how the acquisition dented the fortune of the Tata Steel group:

Tata Steel's failure with Corus and Tata Motors' success with JLR: A tale of 2 buyouts in 9 charts

Rajesh Pandathil and Kishor Kadam

• April 1, 2016, 11:48:00 IST

Jaguar Land Rover, a company that was acquired by Tata Motors in June 2008 for $2.3 billion, offers a contrast to the tale of Tata Steel Europe

Advertisement

"Tata Steel's failure with Corus and Tata Motors' success with JLR: A tale of 2 buyouts in 9 charts")

{kind=link}

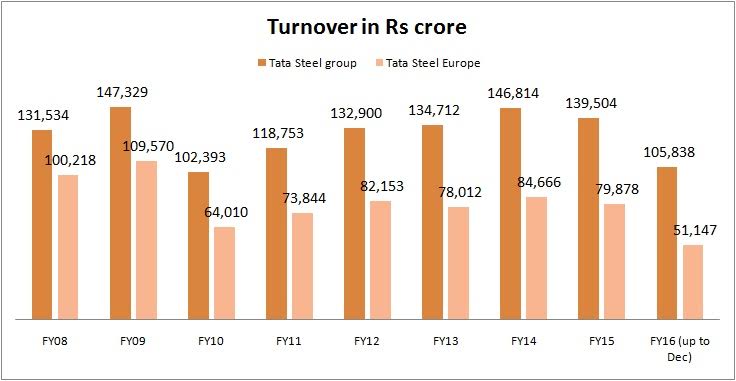

The share of Tata Steel Europe’s turnover in the total turnover of the group has declined steadilty from 2007-08, when it stood at 76.2 percent. In 2014-15, the share was down to 57.3 percent. While Tata Steel group witnessed a 6 percent growth in turnover over the period, Tata Steel Europe saw a 20 percent decline in turnover. Clearly, Tata Steel Europe has been a drag on the group.

{kind=link}

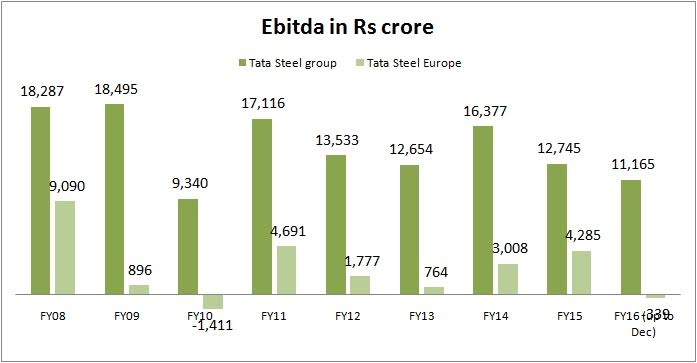

As far as operating profit is concerned, Tata Steel group saw a decline of 30 percent between 2007-08 and 2014-15. Tata Steel Europe, meanwhile witnessed a sharper 53 percent decline. In 2007-08, a year before the global financial crisis started, the foreign subsidiary had a 50 percent contribution to overall Ebitda. The business never went back to that level of operating profit after that. The share in 2014-15 stood at 33.6 percent. In 2015-16 up to December, the group’s consolidated EBITDA stood at Rs 11,165 crore. Tata Steel Europe, meanwhile, reported an operating loss of Rs 339 crore.

{kind=link}

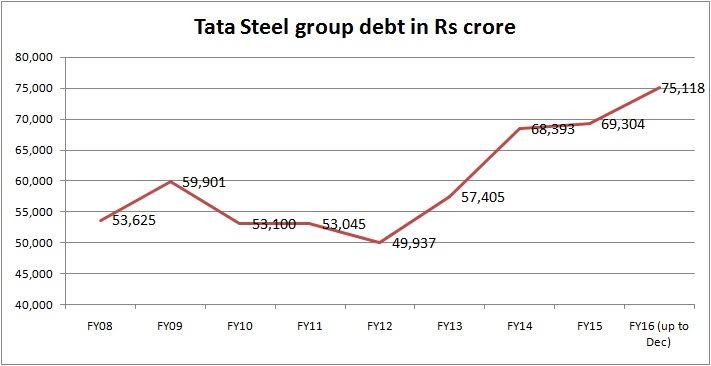

If there is one number that has grown phenomenally for the group, it is debt. From Rs 53,625 crore in 2007-08, it has grown 40 percent to Rs 75,118 crore in 2015-16 (up to December).

{kind=link}

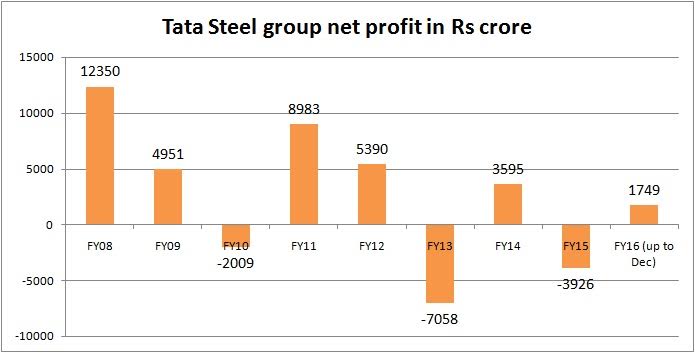

The group’s earnings ever since the acquisition has yo-yoed between profit and loss. In 2007-08, the group registered a net profit of Rs 12,350 crore. This fell 60 percent to Rs 4,951 crore in the next year. Then there was a loss of Rs 2,009 crore and in 2010-11, the group swung back to profit of Rs 8,983 crore. In the course of nine financial years, the group was in profit in 6 times.

{kind=link}

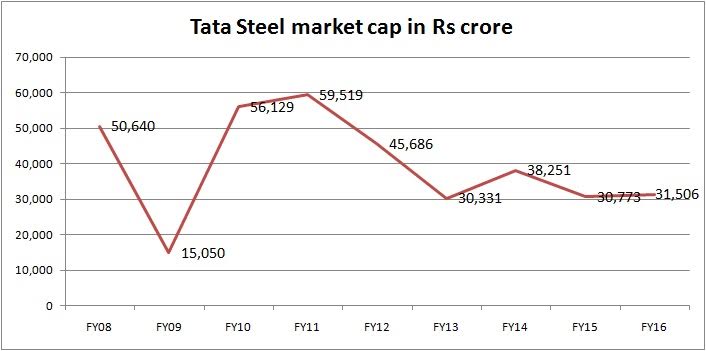

Tata Steel share price on the BSE has more than halved from Rs 693.15 in 2007-08 to Rs 324.4 currently. Its market cap eroded 38 percent during the period from Rs 50,640 crore to Rs 31,506 crore currently. After the company announced the decision to sell the UK business the stock has gained 5.26 percent.

{kind=link}

{kind=link}

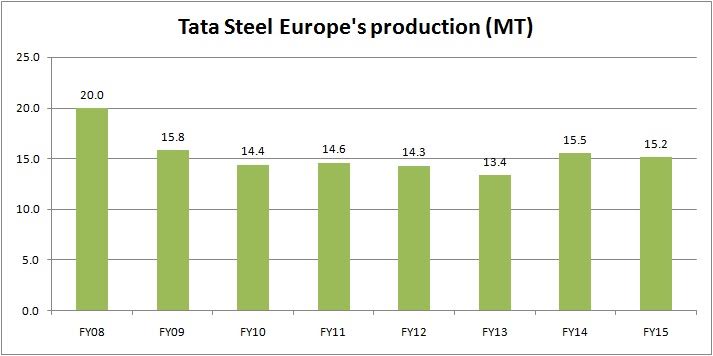

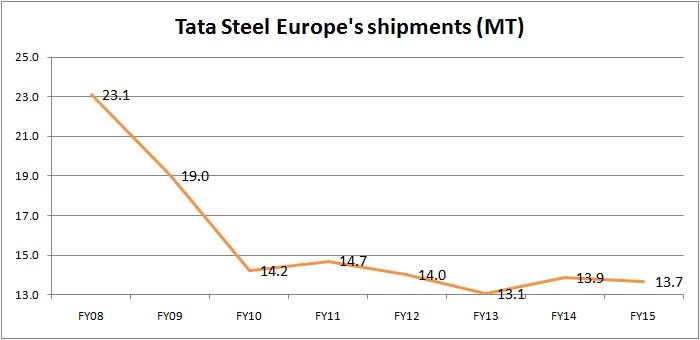

The above two graphics show how the Tata Steel Europe suffered as demand for steel continued to be weak after the global financial crisis. The company’s production never hit 20 million tonne recorded in 2007-08. In fact, the output hovered around 13-15 million tonne for the last seven years. Overall, the output witnessed a 24 percent fall over eight years from 2007-08. Shipments, meanwhile, declined a sharper 41 percent. According to this

article

in Bloomberg citing Gladfly estimates, the European operations have lost almost $5 billion since 2010. Given the ballooning debt of the group, the sale decision does not come as a surprise, says the article. Contrasting story of JLR JLR was acquired by Tata Motors in June 2008 for $2.3 billion, also ahead of the financial crisis. However, the company managed to pull off despite the crippling crisis.

{kind=link}

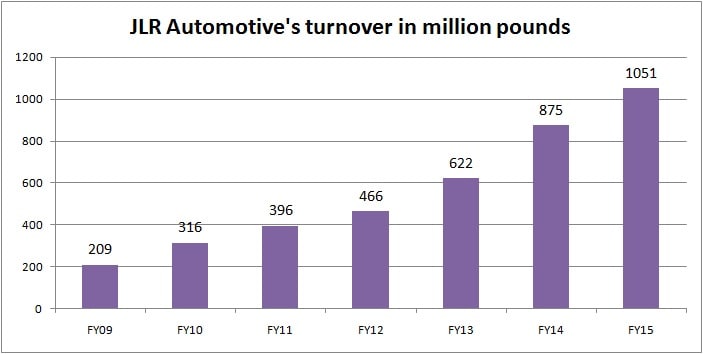

JLR’s turnover has been increasing steadily from 4,949 million pounds in 2008-09 to 21,866 million pounds in 2014-15. In the seven years’ time, JLR has been in operating loss only once - in 2008-09. In 2009-10, the company swung to an operating profit of 51.40 million pounds. This number has been on a steady rise. So is the case with profit after taxes. After the acquisition of JLR, Tata Motors’ consolidated turnover grew 257 percent from 2008-09 to 2014-15. Also the company turned around from a loss of Rs 2,505 crore in 2008-09 to profit of Rs 13,986 crore in 2014-15.

{kind=link}

Interestingly, the common factor in both the stories - one of failure and the other of success - is China. While it is the Chinese dumping that brought Tata Steel down, it is the boom in the Chinese auto market that boosted JLR’s fortunes.

End of Article